Global Markets Face a Critical Week: Inflation Returns, Growth Wobbles

The global economy enters the week of May 18–23 in a Neutral-to-Defensive condition as inflation pressure rises while growth signals become more uneven. The main focus will be on China’s April activity data, UK CPI, Eurozone final inflation, FOMC minutes, global flash PMIs, Japan CPI, Canada CPI, Australia labor data, and UK retail sales.

The U.S. remains the key driver, with markets watching whether the Fed minutes confirm a more hawkish stance after stronger inflation and higher oil prices. China’s data will test whether industrial strength can offset weak consumption and property pressure. Europe and the UK face renewed inflation risk, while Japan’s CPI may increase pressure on the Bank of Japan. Overall, markets will watch whether the global economy is moving toward resilient growth with sticky inflation, or a more dangerous stagflation-risk environment.

US Economy Weekly Review: Resilient Growth, Hot Inflation, and a More Hawkish Fed Risk

The U.S. economy sent a resilient but inflation-heavy signal over the past week, leaving markets with a stronger-dollar, higher-yield, and more selective risk-asset outlook. Growth momentum remained solid, consumer spending stayed positive, manufacturing improved, and GDP tracking strengthened, but the main story was the broad return of inflation pressure across consumer prices, producer costs, trade prices, and energy-linked channels.

April CPI rose 0.6% month-on-month and 3.8% year-on-year, while core CPI also beat expectations at 0.4% monthly and 2.8% annually. Energy was the key driver, with gasoline and broader energy costs rising sharply, reinforcing the impact of the Iran war and Strait of Hormuz disruption on U.S. inflation. Producer inflation was even more concerning: core PPI jumped 1.0% monthly, and headline PPI reached 6.0% annually. Import prices rose 1.9% monthly, while export prices surged 3.3%, showing inflation pressure beyond consumers.

Growth data, however, stayed strong. The Atlanta Fed GDPNow estimate for Q2 increased to 4.0%, retail sales remained positive, and annual retail sales accelerated to 4.87%. Manufacturing also improved sharply, with the NY Empire State index jumping to 19.60, industrial production rising 0.7%, manufacturing production increasing 0.6%, and capacity utilization climbing to 76.1%.

The labor market cooled slightly but did not weaken meaningfully. Initial jobless claims rose to 211K, yet continuing claims fell to 1.782M. Housing also showed resilience, as mortgage applications rebounded despite mortgage rates rising to 6.46%. This suggests households and firms are absorbing higher rates better than expected for now.

Energy data supported the inflation-risk narrative, with crude and gasoline inventories falling more than expected. Treasury auctions showed pressure at the long end, with the 30-year yield rising to 5.050%, reflecting concern about inflation, debt supply, and Fed policy. The Fed backdrop also turned more hawkish, with Kevin Warsh confirmed as Fed Chair and markets pricing higher rate-hike risk.

Overall, the economy is strong, but not in a soft-landing-friendly way. The mix of solid growth, sticky inflation, higher yields, and hawkish policy risk supports USD strength, pressures Treasuries and gold, keeps equities selective, and leaves crypto vulnerable if yields keep rising through the next policy and data cycle.

US Economic Outlook — Week Ahead: May 18–23, 2026

The U.S. economy enters the week of May 18–23 with a more fragile but still resilient macro profile. Inflation pressure has returned clearly, while growth has not yet broken. April CPI rose 3.8% year over year, core CPI increased 2.8%, and energy prices jumped 17.9%. Producer inflation also surprised sharply, with final-demand PPI rising 1.4% month over month and 6.0% annually. Retail sales still increased 0.5% in April, but part of that strength likely reflects higher prices rather than clean real demand.

My base-case view for the week is Neutral-to-Defensive for risk assets, mildly supportive for the U.S. dollar, and volatile for Treasury yields. The key issue is whether housing, labor data, consumer sentiment, and business surveys confirm a harder mix of weaker confidence, higher input costs, and a Federal Reserve with less room to ease.

Monday starts with March foreign portfolio flows, important for judging foreign demand for U.S. assets, Treasuries, and the dollar. Tuesday focuses on housing and wage-structure data, with pending home sales and residential construction still under pressure from high mortgage rates and affordability constraints. Housing starts are expected to slow to around 1.337 million units.

Wednesday’s FOMC minutes are the main policy event. Markets will watch how strongly officials discussed renewed inflation risks, energy pass-through, financial conditions, and whether the next move could still be a cut or potentially a hike. Even with a more hawkish tone, the Fed is likely to prefer holding rates steady while assessing inflation and labor-market effects.

Thursday is the main macro data day, with housing starts, building permits, jobless claims, the Philadelphia Fed index, and S&P Global Flash U.S. PMI. Strong claims and PMI data would confirm resilient growth, but elevated price components could lift yields and the dollar. Friday brings final Michigan sentiment and Fed speeches from Michael Barr and Christopher Waller.

Overall, this is a confirmation week. If housing weakens, sentiment remains depressed, and PMI price pressures stay high, stagflation risk will rise. If claims remain low and PMIs stay above 50, markets may keep pricing resilient growth, but with the Fed trapped in a more hawkish inflation environment.

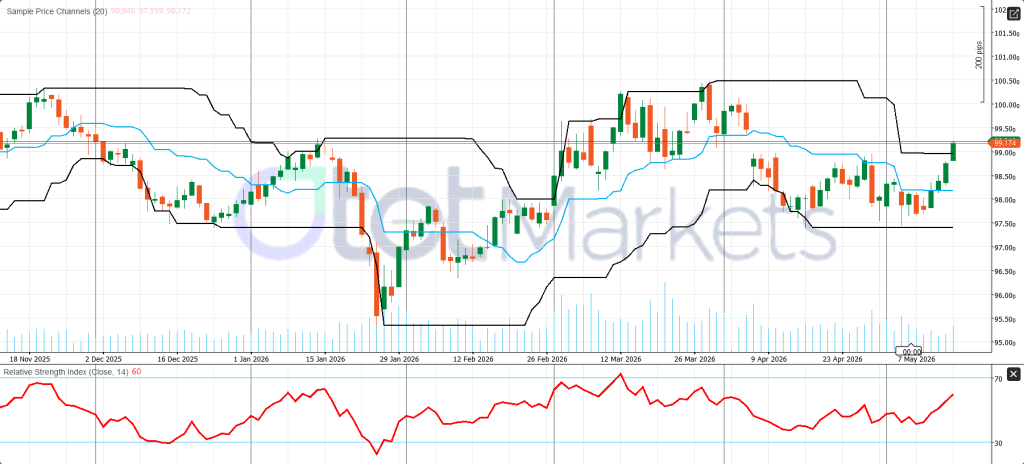

USD Index Technical Analysis

The daily U.S. Dollar Index (DXY) chart has improved and now shows a constructive recovery structure. Price is trading around 99.174, above the 20-day Price Channel upper boundary near 98.946, while the midline is around 98.172 and the lower boundary is near 97.399. Trading above the upper channel suggests that buyers have pushed the index into a short-term breakout attempt rather than a simple range rebound.

The structure has clearly strengthened from the late-April base. DXY has climbed from the lower part of the recent range and is now pressing the next upside area around 99.17–99.50. If the index can hold above 98.95 and extend through 99.50, the next broader resistance comes in near 100.50. On the downside, the first support now stands around 98.17, followed by the more important floor near 97.40.

Momentum also supports recovery. RSI is at 60, which places it above the neutral 50 line and points to improving bullish pressure without yet showing an overstretched market. In practical terms, the chart favors a mildly bullish bias, but the breakout still needs follow-through above 99.50 to look stronger and more durable.

S&P 500 Technical Analysis

The daily S&P 500 / US500 chart remains constructive. Price is trading around 7,402.95, clearly above the 20-day EMA at 7,262.87, which confirms that the broader short-term trend is still pointing higher. The rebound from the late-March low near the 6,300–6,400 zone has already carried the index through the major intermediate levels around 6,600, 6,900, and 7,200.

The key issue now is not trend direction, but extension. Price is pressing the next immediate resistance zone around 7,403, which is the local high on the chart. A clean daily close above that level would strengthen the bullish continuation case and open room toward 7,500 first, followed by the broader upside area near 7,600. On the downside, the first important support comes in around the 20-day EMA near 7,263, while the next broader support sits near 7,200 and then 6,900.

Momentum is still positive, but the market is no longer cheap. RSI is at 66, which keeps it below classic overbought territory but shows that upside pressure remains firm. On-Balance Volume has also risen strongly from the March base, which confirms that the rally has been supported by improving participation rather than a weak drift higher. In practical terms, the chart still favors buyers, but it is now approaching a zone where breakout confirmation matters more than chasing an already-extended move.

China Weekly Review — Selective Recovery, Weak Credit Engine

China’s latest macro picture is mixed: inflation has improved, consumer sentiment has strengthened, and U.S.-China diplomatic headlines have created selective support for aviation, agriculture, AI, and technology trade. However, the core weakness remains the credit cycle. April New Loans fell to -10.0B, far below the 320.0B forecast and sharply weaker than the previous 2,990.0B. Total Social Financing dropped to 620.0B versus the 1,500.0B forecast and the previous 5,230.0B, while outstanding loan growth slowed to 5.6%. This shows that borrowing demand from companies and households is still weak, leaving China’s recovery uneven and not yet broad-based.

The liquidity picture is better but incomplete. M2 Money Stock rose 8.6% year over year, slightly above expectations, meaning liquidity is available. But stronger money supply is not turning into strong lending or investment, which suggests weak policy transmission, cautious business confidence, and fragile private-sector demand.

Inflation data were more constructive. CPI rose 0.3% month over month and 1.2% year over year, beating expectations, while PPI jumped 2.8% annually from 0.5% previously. This reduces deflation concerns, but it also raises margin pressure if input costs rise while final demand remains soft. Consumer sentiment also improved, with the Thomson Reuters IPSOS PCSI rising to 76.34 from 74.60, but sentiment alone cannot offset weak financing demand.

The yuan stayed relatively firm, with USD/CNY near 6.79, helped by summit optimism, policy confidence, and relative macro stability. The U.S.-China summit added positive headlines around trade, tariffs, AI, rare earths, agriculture, aviation, and Iran, although limited details and weak discussion on chip controls reduced hopes for a major breakthrough. Nvidia’s reported approval to sell H200 AI chips to 10 Chinese companies was supportive for AI sentiment.

Alibaba’s results reinforced the strength of China’s AI and cloud sectors, with Cloud Intelligence revenue up 38% and AI-related revenue posting another quarter of triple-digit annual growth. The Boeing order for 200 jets also supported diplomatic sentiment, though it was below expectations.

Overall, China is improving selectively, but weak credit data show the recovery is not yet a full-cycle acceleration. Policy support may continue, but stronger credit demand is needed for broader sustainable momentum.

China Economic Outlook — Week Ahead: May 18–23, 2026

China enters the week of May 18–23 with a mixed macro setup. Headline growth has remained resilient, but domestic demand, credit appetite, and property activity are still weak. The main question is whether April activity data confirm deeper weakness in consumption and investment, or whether industrial production and external trade remain strong enough for Beijing to avoid broad stimulus.

My base-case view is Neutral-to-Defensive for Chinese equities, cautious for the yuan, and selectively supportive for commodities only if industrial output and fixed-asset investment remain firm.

The key event comes on Monday, May 18, with China’s April activity data: industrial production, retail sales, fixed-asset investment, real estate development and sales, home prices, and urban unemployment. Industrial production remains the main stabilizer. March output rose 5.7% year over year, slower than 6.3% in January–February but still above expectations. A strong April reading would support the factory-resilience story, while a weak figure would raise concerns over energy costs, export uncertainty, and softer global demand.

Retail sales are the most important domestic-demand signal. March sales rose only 1.7% year over year, down from 2.8% in January–February. If April remains weak, it will confirm cautious household behavior despite policy support. Fixed-asset investment also matters after rising just 1.7% in Q1, with infrastructure and manufacturing helping but real estate still dragging.

Property remains the biggest structural risk. Weak home prices, falling investment, or poor sales would increase pressure for targeted support for developers, mortgages, local-government financing, and household demand. Urban unemployment will also be important because labor weakness would reinforce the cautious-consumer narrative.

The second key event is the Loan Prime Rate decision on Wednesday, May 20. Markets expect the one-year LPR to stay at 3.00% and the five-year LPR at 3.50%. The PBOC needs to support growth, but aggressive easing is constrained by yuan sensitivity and external inflation pressure.

April credit data showed weak borrowing demand, with new yuan loans contracting by 10 billion yuan and household loans falling 786.9 billion yuan. Meanwhile, PPI rose 2.8% and CPI 1.2%, reducing deflation fears but raising margin-pressure risks.

Overall, China remains a selective recovery story, not a full-cycle acceleration.

USD/CNH Technical Analysis

USD/CNH still shows a broader bearish structure, despite a short-term stabilization attempt near 6.8127. The pair is holding just above the 6.78–6.80 support zone, but the larger trend from the January peak remains defined by lower highs and lower lows. Although price has moved back above the descending trendline from the late-2025 to early-2026 decline, the rebound lacks enough follow-through to confirm a durable bullish reversal.

The immediate outlook is mixed but still downside biased. Resistance is first seen near 6.90, with a stronger ceiling around 7.15. A clear break below 6.80 would show 6.70 as the next support. As long as USD/CNH stays below 6.90, the move looks more like a corrective bounce than a trend change.

Momentum supports caution: OBV remains weak, and RSI near 45 shows limited upside strength. Selling rallies still looks favored.

Gold Market Condition and Weekly Outlook — May 18–23, 2026

Gold enters the week of May 18–23 in a corrective phase, with short-term sentiment still weak after four consecutive daily losses. XAU/USD is trading around $4,540/oz, with the recent range near $4,511–$4,666. Comex gold ended the week down 3.49% at $4,555.80, its largest weekly decline since March 2026. The overall market condition is Neutral-to-Sell, with a clear sell-on-rallies bias unless gold recovers above the $4,700 area.

Gold’s weakness does not mean geopolitical risk has disappeared. The U.S.-Iran conflict, fragile ceasefire, and continued concerns around the Persian Gulf and Strait of Hormuz still provide a support floor. However, safe-haven demand has not been strong enough to offset pressure from the U.S. macro side.

The main bearish driver is the U.S. inflation shock. April CPI rose 0.6% MoM and 3.8% YoY, while core CPI increased 0.4% MoM and 2.8% YoY. Producer inflation was even stronger, with headline PPI at 6.0% YoY and core PPI up 1.0% MoM. Import prices rose 1.9%, and export prices climbed 3.3%. This broad inflation pressure reduced expectations for near-term Fed easing and increased the probability of tighter-for-longer policy.

The U.S. dollar is the second major headwind. The Dollar Index rose to around 99.20, its strongest level in more than a month. A stronger dollar makes gold more expensive for non-U.S. buyers, while higher Treasury yields increase the opportunity cost of holding a non-yielding asset.

Technically, gold remains under pressure. Price failed to hold above $4,700, broke below $4,650–$4,680, and moved toward $4,540–$4,555. Immediate support is around $4,510–$4,500. A break below that zone could expose $4,450, then $4,380–$4,400. Resistance stands at $4,600, followed by $4,650–$4,700.

The daily chart is also weak, with price below all three Alligator lines. The key technical pivot is $4,540. A close below $4,500 would increase downside risk toward $4,400 and $4,300. Overall, gold remains a strategic hedge, but the short-term setup still favors selling rallies unless U.S. data weaken sharply or geopolitical risk escalates.

Energy Market Weekly Outlook — May 18–23, 2026

WTI enters the week of May 18–23 in a bullish but highly volatile condition, driven mainly by supply risk rather than normal demand strength. Oil prices remain elevated as the Strait of Hormuz disruption, the fragile U.S.-Iran ceasefire, and deeper-than-expected U.S. inventory draws continue to support a geopolitical risk premium. WTI closed near $105.42/bbl on May 15, up 4.2% on the day and around 10% for the week after rising from about $95.42 on May 8.

The rally is primarily a Persian Gulf supply-risk story. Markets are pricing restricted flows through Hormuz, disrupted tanker traffic, higher insurance and shipping costs, and faster inventory drawdowns. The EIA expects Hormuz to remain effectively closed through late May, forcing global inventories to fall by about 2.6 million barrels per day this year, while Brent may average around $106/bbl in May and June.

The disruption remains severe. Before the war, roughly 20% of global oil supply moved through the Strait of Hormuz. Saudi Aramco CEO Amin Nasser warned that normalization could take until 2027 if the disruption lasts beyond mid-June. He said more than 600 ships were stuck in the Persian Gulf, around 240 ships were waiting outside Hormuz, and only 2–5 ships were passing daily versus about 70 before the war.

U.S. inventories reinforced the bullish setup. API reported a 2.188 million-barrel crude draw, while the official EIA report showed crude stocks down 4.306 million barrels, Cushing inventories down 1.702 million, and gasoline stocks down 4.084 million. This is especially important before the U.S. summer driving season. U.S. producers are responding, with the oil rig count rising to 415, but new rigs cannot quickly offset a major geopolitical supply shock.

The inflation impact is already visible. Energy prices contributed heavily to April U.S. CPI, reducing expectations for near-term Fed easing and supporting higher yields and a stronger dollar. This could pressure commodities indirectly, but oil remains dominated by supply risk.

This week, the EIA petroleum report, FOMC minutes, U.S. macro data, Michigan sentiment, and Baker Hughes rig count will shape short-term direction.

Technically, WTI remains constructive. Price is above key Fibonacci levels at $95.216, $87.682, and $80.148. Holding above $95.216 keeps the bullish recovery bias intact, with upside targets near $105, $110, and possibly the prior high around $119.607. Overall, WTI remains Buy but volatile, with dips likely to attract buyers while chasing spikes remains risky.

Crypto Market Weekly Outlook — May 18–23, 2026

The crypto market enters the week of May 18–23 in a defensive but not broken condition. Bitcoin remains the main stabilizer, but short-term momentum has weakened as hot U.S. inflation, a stronger dollar, higher Treasury yields, and renewed geopolitical risk continue to pressure risk assets. The overall market condition is Neutral, while the BTC outlook is Neutral-to-Buy only if key support holds. Altcoins remain selective and high-risk.

Bitcoin has recently traded around $78,970–$81,100, after failing to hold cleanly above the $80,000–$82,500 resistance zone. Holding near $80,000 has prevented a deeper bearish breakdown, but the failure to sustain the move toward $82,000–$82,400 shows that buyers are not yet strong enough to create a broad risk-on breakout.

The main pressure comes from U.S. macro data. April CPI rose 0.6% MoM and 3.8% YoY, while core CPI increased 0.4% MoM and 2.8% YoY. Producer inflation was stronger, with headline PPI at 6.0% YoY and core PPI up 1.0% MoM. This is negative for crypto because stronger inflation reduces expectations for near-term Fed easing and raises the risk of tighter policy later this year.

The U.S. dollar is another headwind. The Dollar Index rose to around 99.20, its strongest level in more than a month. A firmer dollar usually pressures Bitcoin and altcoins by reducing global liquidity appetite. Fed risk also increased after Kevin Warsh’s confirmation as Fed Chair and his pledge to shrink the Fed’s $6.7T balance sheet, which matters because crypto is highly sensitive to liquidity expectations.

Ethereum underperformed Bitcoin, trading around $2,224–$2,300, while most altcoins stayed under pressure. This confirms that risk appetite remains fragile.

The main positive theme is regulation. The U.S. Senate Banking Committee is moving forward with the CLARITY Act, which could support long-term institutional confidence. Institutional demand also remains supportive, with CoinShares reporting $857.9 million inflows, including $706.1 million into Bitcoin, although spot ETF flows remain volatile.

Technically, BTC support is $75,000–$78,000. A break below $75,000 would shift the outlook toward Neutral-to-Sell. On the upside, BTC must reclaim $82,000–$82,500 to restore bullish momentum and open the way toward $85,000–$88,000.

Share

Hot topics

What Is a Breakout Trading Strategy and How to Trade It?

If you have ever observed a price move quietly for some time and then suddenly move in a particular direction, you have already seen a breakout in action. Breakouts can...

Read more

Submit comment

Your email address will not be published. Required fields are marked *