China’s Manufacturing Activity Rebounds in June

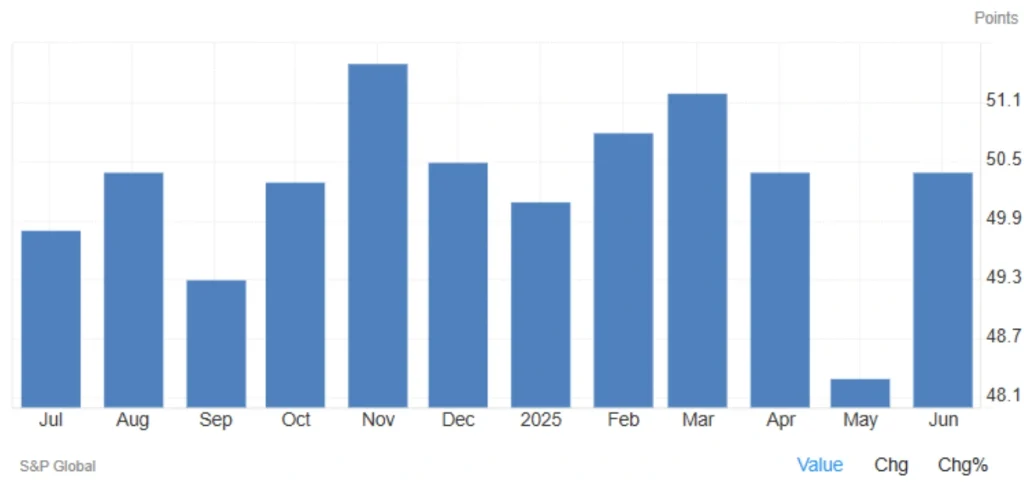

China’s Caixin Manufacturing PMI jumped unexpectedly to 50.4 in June 2025, rising sharply from 48.3 in May, its lowest point since September 2022. This reading beats market expectations of 49.0 and marks a return to expansionary territory for the first time in three months.

Key Highlights:

- Caixin PMI (June): 50.4 → Above the 50-mark, indicating growth

- Previous Month: 48.3 → Sharp contraction

- New export orders: Fell for the third consecutive month

- Domestic production: Logged the fastest growth since Nov 2024

- Input prices: Declined for the fourth straight month

- Output prices: Fell for the seventh month, with the steepest drop in five months

Educational Note: What is the Caixin Manufacturing PMI?

The PMI (Purchasing Managers’ Index) is a forward-looking economic indicator based on surveys of purchasing managers. It reflects business conditions across key areas such as output, new orders, prices, and employment.

Unlike the official government PMI, the Caixin PMI focuses more on small and medium-sized private firms and is often used as a complementary indicator for a more nuanced view of China’s economy.

- PMI above 50 = Expansion

- PMI below 50 = Contraction

Market Impact & Interpretation

This rise above the 50-point mark is the first sign of recovery in China’s private manufacturing sector in three months.

However, the rebound appears to be driven primarily by domestic demand, not by export growth. New export orders continued to decline, likely a result of higher U.S. tariffs on Chinese goods, suggesting that external trade remains a drag.

Meanwhile, input and output prices have declined for multiple months, pointing to reduced inflationary pressure in the manufacturing sector. While this could make Chinese exports more competitive, it also indicates shrinking profit margins for producers.

🧨 Business confidence remains weak, with sentiment below its long-term average, reflecting persistent caution about a sustainable recovery path.

Read More: China’s Industrial Growth Slows in May 2025

Final Summary & Forward Outlook

The rise in the Caixin Manufacturing PMI above 50 signals an initial phase of industrial recovery for China’s private sector.

However, continued weakness in exports, soft job market conditions, and falling prices point to a fragile and uneven rebound.

Possible Scenarios

📌 Optimistic Case:

If China continues fiscal and policy support, and if U.S.-China trade tensions ease, the domestic recovery could strengthen and become more balanced, lifting the broader Asian markets and supporting the Chinese yuan and commodity-linked currencies like the Australian dollar.

📌 Pessimistic Case:

Without export recovery or clear government stimulus, China could face a limited internal recovery with ongoing pressure on manufacturing margins, potentially weighing on Asian equities and global commodity demand.

Share

Hot topics

What Is Liquidity in Trading Strategy?

Liquidity plays a role in price execution when trading. You may have noticed the price came in worse than you expected and have already experienced liquidity at work without realizing...

Read more

Submit comment

Your email address will not be published. Required fields are marked *