The last week and the first week in one glance!

The global economic outlook for 2025 remains uncertain. Recent data highlight sustained global momentum, though Europe faces challenges, and optimism surrounds China’s recovery. The Japanese yen’s continued weakening raises concerns about Japan’s trade conditions, particularly following the central bank’s decision to maintain its policy rate. Balancing inflation control with easing pressures on rate-sensitive sectors will remain a key focus of monetary policy in 2025.

As anticipated, the Federal Open Market Committee (FOMC) reduced the federal funds rate target by 25 basis points this week, marking a cumulative 100 bps reduction from its peak of 5.25%-5.50% through successive cuts in September, November, and December.

USA – USD and Wall Street

Last week ended with stress across the US, with tensions about a government funding bill. The US Congress passed a government funding bill early Saturday, narrowly avoiding a shutdown that could have disrupted the holiday season. The Senate approved the bill 38 minutes after the previous funding expired, with bipartisan support in both chambers. The legislation extends funding until March 14, allocates $100 billion for disaster relief, and $10 billion for farmers, and extends farm and food aid programs.

Key provisions, such as limits on investments in China and a pay raise for lawmakers, were removed following opposition from former President Trump and billionaire Elon Musk. Democrats expressed concerns over Musk’s influence and its impact on the legislation.

The bill passed despite resistance from some Republicans who criticized the lack of spending cuts. Speaker Mike Johnson emphasized that Republicans would have greater control in future budget decisions when they gain majorities and Trump assumes the presidency.

A shutdown could have cost the travel industry $1 billion per week, caused airport delays, and disrupted federal services. Congress still faces challenges, including raising the debt ceiling and managing the national debt of over $36 trillion.

Looking at economic data, we can say that the U.S. economy has outperformed recession forecasts, driven by strong consumer spending, which has boosted GDP growth but slowed progress on reducing inflation. In Q3, GDP growth was revised up to 3.1% annualized, supported by robust consumer spending and exports. Final demand indicators, including real personal consumption and business investment, show continued strength.

Data for Q4 reveals resilience, with retail sales beating expectations for six consecutive months and holiday sales up 3.5% year-to-date. Personal spending grew 5.5% year-over-year in November, supported by steady income growth despite cooling wages as hiring demand eases.

Labor cost growth has slowed, reducing inflationary pressures from the labor market. However, consumption remains strong, keeping core inflation steady at 2.6%-3.0% annually throughout 2024. In response, the Federal Reserve cut rates by 25 bps to 4.25%-4.50% but signaled a potential pause in further rate cuts to strike a balance between controlling inflation and supporting rate-sensitive sectors.

The final week of 2024 offers limited data due to the holiday season, but notable housing market updates and durable goods orders are available:

- Building Permits (Nov): Expecting to increase by 1.505M, surpassing the previous 1.419M, with a 6.1% month-over-month rise compared to a 0.4% decline in October.

- New Home Sales (Nov): Supposed to rise by 650K, exceeding the prior figure of 610K, signaling continued strength in the housing market.

- Durable Goods Orders (MoM) (Nov): We expect a -0.4% decline, reversing from the 0.2% growth in October, indicating potential cooling in demand for long-lasting manufactured goods.

These figures highlight resilience in the housing market but hint at mixed signals in broader economic activity.

The first week of 2025 is expected to bring a mix of positive and cautious economic data. The ISM Manufacturing Index has been signing contractions for most of the past two years, and December is likely to follow the same trend, reflecting the sector’s struggles to gain momentum. Uncertainty surrounding the Trump administration’s tariff policies is expected to keep purchasing managers hesitant, delaying significant recovery. However, contingency plans to counter potential tariff pressures could drive some short-term activity. On the other hand, the ISM Services Index remains in expansion territory despite a slight pullback in November. The service sector continues to show resilience, but policymakers face the challenge of managing its growth without overly restricting manufacturing and other interest-rate-sensitive parts of the economy.

The December employment report, due on January 10, is expected to show payroll growth returning to its recent trend after weather and strikes caused fluctuations in prior months. Hiring has averaged 140,000 per month over the past six months, a significant slowdown from earlier in 2024 when monthly gains averaged 220,000. While the pace of hiring has moderated, it hasn’t collapsed. Layoffs remain low, and unemployment claims are stable, reflecting a cooling but resilient job market. Wage growth has also eased, reducing inflationary pressures, with December wages expected to rise modestly by 0.2%.

Looking ahead, hiring is projected to slow further in 2025. The Federal Reserve, acknowledging the labor market’s resilience, appears comfortable taking a slower approach to policy adjustments. With inflationary pressures easing and consumer spending holding up, the Fed aims to balance its focus on curbing inflation while allowing the economy to maintain its momentum.

The U.S. dollar is likely to remain stable with a slight downside bias in early 2025. The Federal Reserve’s recent 25-basis-point rate cut and signals of a slower pace of policy adjustments suggest limited upward momentum for the dollar, particularly as inflationary pressures ease and wage growth moderates. However, the dollar’s resilience will be supported by the ongoing strength in consumer spending and the U.S. economy’s overall momentum, as reflected in better-than-expected Q3 GDP revisions and steady ISM Services data. Weakness in ISM Manufacturing and slower labor market gains may weigh on the dollar, especially if global risk appetite improves, leading investors to seek opportunities outside the USD. From the technical point of view, 106.80 is the key support, then 106.00 and 105.50 as for the targets in the last days of 2024 and the beginning of 2025, which from our point of view confirms the strong USD.

On Wall Street, the outlook remains cautiously optimistic. The cooling labor market and subdued wage pressures offer hope for corporate margins, while resilient consumer spending and solid holiday retail sales are likely to support equities, particularly in sectors like consumer discretionary and technology. That said, headwinds remain, especially for manufacturing and rate-sensitive sectors, which could struggle amid uncertainty surrounding trade policies and ongoing global economic challenges. Investors will focus on incoming data, particularly employment figures and ISM reports, for signs of continued economic resilience or softening demand. A steady labor market with controlled inflation could pave the way for a positive start to 2025 for Wall Street, though sentiment may remain cautious as uncertainties around tariffs and slower global growth linger. From the technical point of view, US500 holding above 5,880 remains bullish. We expect Santa Rally to hold the prices higher in the last days of 2024, but we cannot guarantee that as a positive beginning in the New Year Trading season.

Eurozone and Euro, Current State and Outlook

The Eurozone continues to grapple with a mixed economic backdrop as inflationary pressures ease but growth concerns persist. ECB President Christine Lagarde’s recent remarks suggest a dovish shift in monetary policy, signaling that the central bank is leaning toward further interest rate cuts. Her assertion that “the darkest days of winter look to be behind us” reflects optimism about taming inflation but also acknowledges the challenges posed by a weak growth outlook. This dovish stance aligns with the lower-than-expected HICP inflation rate for November, which further bolsters the case for easing monetary policy.

From a macroeconomic perspective, Germany’s and France’s manufacturing PMI figures have deteriorated further into contraction territory, highlighting ongoing struggles in the bloc’s largest economies. These weak PMI results, coupled with subdued ZEW and IFO surveys, underscore the fragile sentiment among businesses and investors, driven by slowing demand and persistent structural challenges. While services PMI figures have held up relatively better, the broader economic narrative remains concerning.

In the final week of 2024, market activity will likely remain subdued due to the holiday period, but the data releases, such as durable goods orders and U.S. employment figures, may indirectly impact the Euro’s performance through the EUR/USD pair, as we have no data to watch the Eurozone. With limited major Eurozone-specific data expected, the focus will likely remain on broader market sentiment and central bank narratives.

As we move into the first week of 2025, the outlook for the Euro remains tied to expectations of further monetary easing. PMI data set to be released could provide fresh insights into the manufacturing and services sectors, potentially reinforcing concerns about sluggish growth. However, if sentiment surveys, such as the ZEW and IFO, show signs of stabilization or improvement, it may temper some of the bearish sentiment surrounding the Euro.

The Euro is expected to face downward pressure in the near term, particularly if ECB signals of rate cuts strengthen and U.S. economic data continues to outperform. On Wall Street, easing inflation in the Eurozone could be seen as a global growth-positive development, but persistent weakness in Eurozone economic indicators may dampen investor appetite for European equities, maintaining a divergence between U.S. and Eurozone markets.

From the technical point of view, EURUSD remains bearish, especially with trading under 1.06 with strong support at 1.03, which if breached, then we can expect much lower digits even under the 1.00 psychological rate.

Gold!

Gold’s outlook for the rest of 2024 remains optimistic, and setting a target of 2,700 USD appears achievable given both the market dynamics and technical analysis.

The Federal Reserve’s recent actions have played a significant role in shaping the current environment for gold. While the Fed’s latest 25-basis-point rate cut was in line with prior expectations, their more cautious approach to future rate cuts took traders by surprise. This shift in the Fed’s stance caused a strong rally in the US Dollar, which led to heavy selling in gold futures. Gold’s highly leveraged nature magnified the effects of this rally, intensifying the selling pressure. Despite this short-term drop, the long-term bullish trend for gold remains intact.

Since September, speculators have significantly reduced their long positions in gold, which could provide further support for its price shortly. While the recent price drop has raised some concerns, the fundamental outlook for gold remains strong. The outlook for gold stocks is also promising, with substantial profit growth anticipated in the coming quarters. Despite the short-term fluctuations, gold’s long-term uptrend is expected to continue.

As we approach the end of the year, there are additional factors that could contribute to gold’s upward movement. With cash outflows from stocks and risky markets, some of this capital is likely to be redirected towards gold, driven by its safe-haven status. In times of economic uncertainty, investors tend to seek refuge in assets like gold, which are perceived as more stable.

From a technical perspective, 2,620 USD is a key pivot for gold. If this level holds, the next target will likely be 2,660 USD, with the potential to reach 2,700 USD by the end of 2024. The outlook remains bullish, and the path to 2,700 USD appears increasingly likely, especially as gold continues to benefit from its safe-haven appeal amidst global uncertainty.

Oil

Oil prices ended last week largely unchanged, with markets assessing Chinese demand and expectations of interest rate cuts following data showing cooling U.S. inflation. Both oil benchmarks dropped around 2.5% for the week. The U.S. dollar retreated from a two-year high but remained on track for its third consecutive week of gains after the Federal Reserve cut interest rates and trimmed its outlook for future rate cuts. A stronger dollar can make oil cheaper for foreign buyers, and rate cuts could boost oil demand.

Concerns persist over the demand outlook, particularly in China, where state-owned refiner Sinopec forecasted that China’s crude imports could peak by 2025, and oil consumption might peak by 2027. Additionally, the U.S. monetary policy’s potential shift has raised worries. OPEC+ has emphasized the need for supply discipline to stabilize prices as it revised its 2024 oil demand forecast down for the fifth consecutive month.

JPMorgan predicts the oil market will shift from a balance in 2024 to a surplus in 2025 due to increased non-OPEC+ supply and steady OPEC output. On the geopolitical front, U.S. President-elect Donald Trump hinted at potential tariffs on the European Union if it doesn’t reduce its deficit with the U.S. through oil and gas trades. Meanwhile, G7 countries are considering tightening the price cap on Russian oil, as Russia has evaded the $60 per barrel cap with its “shadow fleet” of ships.

In the futures market, money managers raised their net long positions in U.S. crude for the week ending Dec. 17.

Fundamental data are natural for now, we have nothing special to say that for this reason, we will have a big change in the price levels unless geopolitical tensions prove otherwise. This side movement is also confirmed by technical indicators, where we have the main support and resistance as the lower and higher band of this side movement at 72 and 67 USD respectively. Any big move, higher or lower, needs to pass these mentioned levels.

BTC

Bitcoin experienced a sharp decline, falling towards $92,000 from its peak of over $108,000. As the market struggles with a change in momentum, a retracement is looming on the horizon. Although some people may find the price correction concerning, there are important trends and dynamics to keep an eye on that suggest what Bitcoin may do next.

The chart shows that Bitcoin has experienced a significant uptrend since October, as indicated by the rising price action and the upward slope of the 50-day Exponential Moving Average (EMA, blue line). Recently, there has been a pullback in the price, with the latest candle showing a slight recovery. The price is currently testing the 20-day EMA, which has been acting as support throughout the uptrend.

The EMA is currently at approximately 99,220, which is slightly above the current price, indicating that the EMA might act as dynamic resistance in the short term.

There was a spike in volume during the recent price drop, suggesting strong selling pressure. However, the volume has decreased slightly in the latest candle, coinciding with the price stabilization.

The Accumulation/Distribution Line indicator has been trending upwards, which generally suggests accumulation. However, a slight plateau or dip coincides with the recent price drop, indicating a possible slowdown in buying pressure or an increase in selling pressure.

The immediate resistance can be seen around the 50-day EMA level (approximately 99,220). Further resistance might be found near the recent high of around 110,000. The nearest support level could be around the recent low of approximately 97,175. If the price breaks below this level, the next significant support might be around the 90,000 level, where previous price consolidations occurred in November.

The chart does not show clear classical chart patterns like head and shoulders, triangles, etc., within the recent price action. However, the pullback to the 20-day EMA (around 94K) could be seen as a test of this key support level in an ongoing uptrend.

The current situation suggests a critical juncture where Bitcoin is testing the 50-day EMA as support. The outcome of this test could determine the short-term trend direction. If the EMA holds as support and the price rebounds, it could signal a continuation of the uptrend. Conversely, the break below could indicate a deeper correction. Monitoring the volume and the Accumulation/Distribution line will provide further clues about the strength of the current price level.

Submit comment

Your email address will not be published. Required fields are marked *

Share

Hot topics

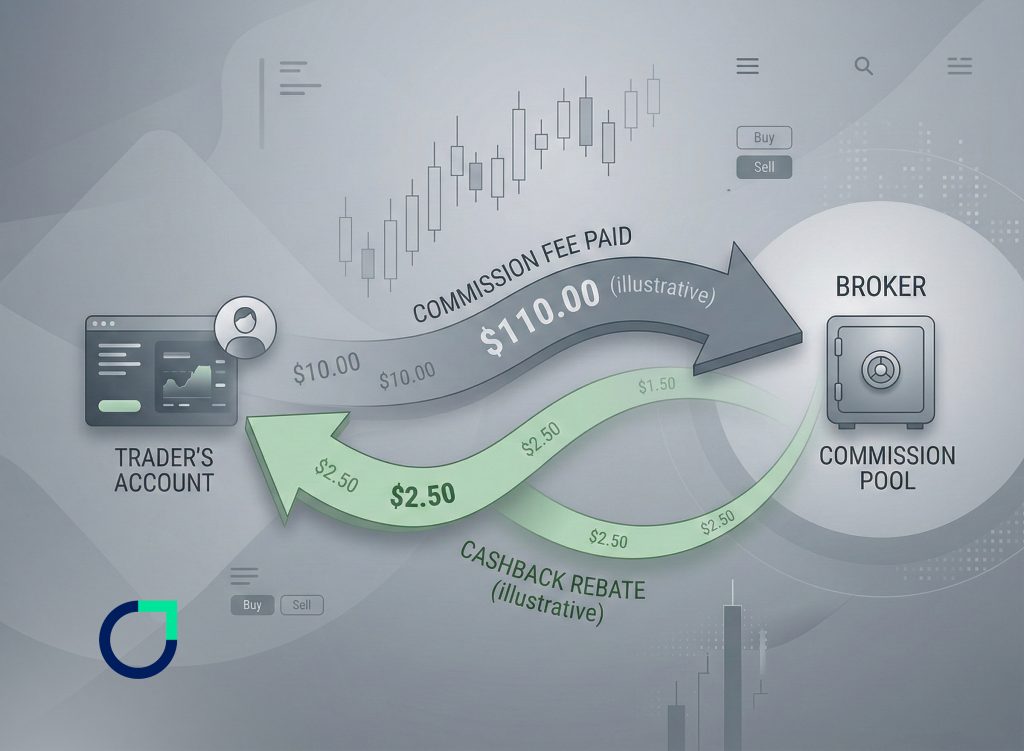

What is Forex Rebate

Introduction If you have been trading Forex for a while, you have probably noticed that every trade comes with a cost. Whether it is spread, commission, or both, trading is...

Read more

Comments (1)