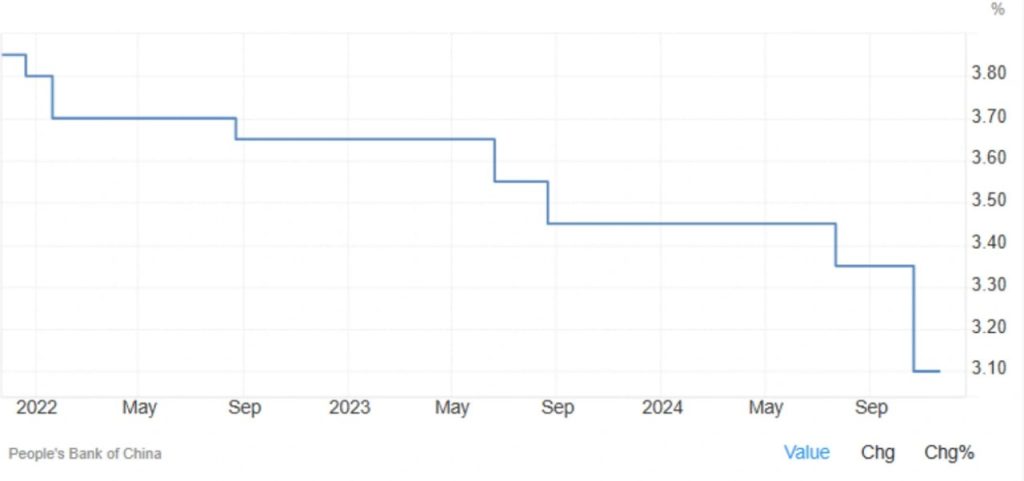

PBoC Holds Key Lending Rates Steady in November 2024

In its November 2024 fixing, the People’s Bank of China (PBoC) decided to keep its key lending rates unchanged, aligning with market expectations. The one-year loan prime rate (LPR), which serves as the benchmark for most corporate and household loans, was retained at 3.1%. Meanwhile, the five-year LPR, which is typically used as a reference for property mortgages, remained steady at 3.6%. Both of these rates are at historically low levels, following reductions in October and July. The PBoC’s decision to maintain the current rates reflects its ongoing approach to managing the Chinese economy, signaling a cautious approach in the face of continued economic challenges.

A Delicate Balancing Act: Stimulus Measures and Economic Targets

The PBoC’s decision comes as the Chinese economy grapples with a range of challenges, including a prolonged downturn in the property sector, low consumer and business confidence, and ongoing deflation risks. The central bank’s move to maintain the key lending rates underscores its commitment to providing stable financial conditions while evaluating the effectiveness of existing stimulus measures. Since late September, Beijing has ramped up efforts to counter the economic slowdown, aiming to achieve the 2024 growth target of approximately 5%. Despite these efforts, the property sector remains weak, and there are significant deflationary pressures that continue to weigh on consumer spending and business investment.

The PBoC’s decision to keep interest rates steady reflects a cautious approach, acknowledging that additional rate cuts or easing measures could be implemented if the economic recovery remains sluggish. While the rate cuts earlier in the year were designed to support economic activity, the central bank is continuing to monitor both domestic and global economic conditions to ensure that its monetary policy remains aligned with broader growth objectives. This approach indicates that the PBoC is carefully navigating its monetary policy tools, maintaining support for the economy while avoiding overly aggressive moves that could lead to undesirable side effects.

Property Sector Weakness and Deflation Risks

One of the primary concerns facing the Chinese economy is the ongoing weakness in the property sector, which has struggled to recover from a prolonged period of downturn. The real estate market, a key driver of China’s economic growth in recent years, remains under pressure from a combination of sluggish demand, mounting debt issues, and tightening regulations aimed at curbing speculative investments. As a result, the PBoC and Chinese policymakers are under increasing pressure to find ways to stabilize the sector and restore investor confidence.

At the same time, deflation remains a significant risk to the economy, with low consumer and business confidence contributing to subdued demand. Deflationary pressures can be particularly harmful, as they may lead to a cycle of reduced spending and investment, further exacerbating the economic slowdown. The central bank’s decision to hold rates steady at this time suggests that it is continuing to monitor these risks closely, with the goal of supporting demand and encouraging a more robust recovery in the broader economy.

Future Policy Easing Expected as PBoC Monitors Economic Conditions

Looking ahead, the PBoC is widely expected to implement additional policy-easing measures if economic conditions do not improve as hoped. The central bank has already indicated its readiness to act further, with Governor Pan Gongsheng mentioning in October that the PBoC might consider reducing the reserve requirement ratio (RRR) by 25 to 50 basis points by the end of the year, depending on liquidity conditions. Such a move would be aimed at freeing up more cash for banks to lend to businesses and consumers, providing additional stimulus to the economy.

Given the continued economic headwinds and uncertainty surrounding global markets, the PBoC’s stance on monetary policy remains fluid. While the central bank has taken a wait-and-see approach with interest rates for now, it is clear that it stands ready to implement more aggressive measures if necessary. Analysts and market participants will be closely watching any future announcements from the PBoC, particularly in relation to the property sector, deflation risks, and the overall economic growth trajectory. The effectiveness of the central bank’s stimulus measures in the coming months will be critical in determining whether China can meet its growth target and navigate through these challenging economic conditions.

Share

Hot topics

Gold symbol in forex

Introduction If you have ever opened a trading platform and searched for gold, you probably noticed a specific code instead of the word “gold.” In the forex world, assets are...

Read more

Submit comment

Your email address will not be published. Required fields are marked *