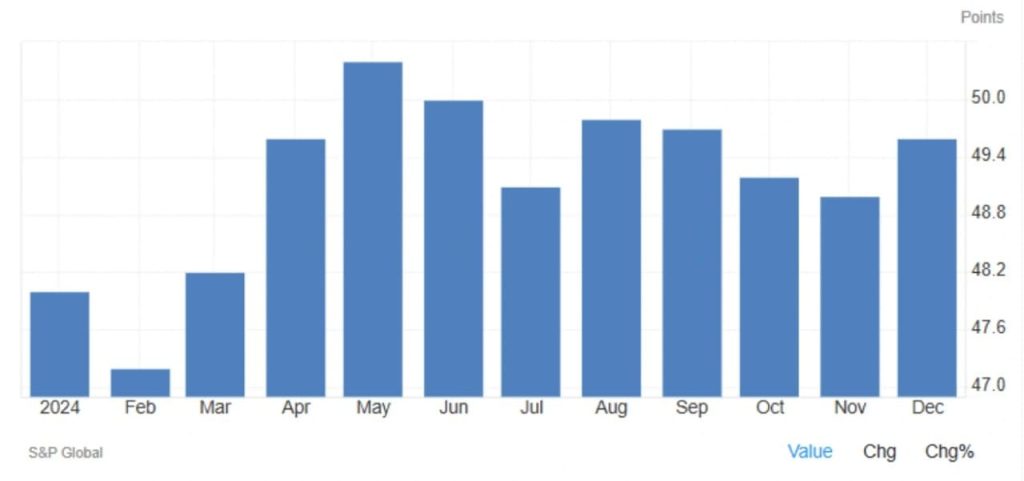

Japan’s Manufacturing PMI Shows Modest Improvement

In December 2024, Japan’s au Jibun Bank Manufacturing PMI stood at 49.6, slightly above the flash estimate of 49.5 and an improvement from the 49.0 recorded in November. While the PMI remained below the neutral 50.0 mark, indicating a continued contraction in factory activity, the rise in the index pointed to a milder pace of decline compared to previous months. This marks the highest reading since September, suggesting that despite ongoing challenges, there may be signs of stabilization in the sector.

Milder Contraction in Output and Stabilizing Orders

Japan’s Manufacturing PMI continued to face contraction in December, but the rate of decline in output softened significantly. The drop in production became marginal, indicating that the worst of the contraction may have passed. Similarly, new orders, while still declining, saw their rate of reduction ease to the slowest pace in six months. This shift suggests a possible stabilization in demand, though it is too early to determine whether it will result in a full recovery. New export orders, however, remained subdued, pointing to ongoing challenges in international markets, particularly in light of global economic uncertainties.

Employment in the manufacturing sector showed signs of improvement as it reversed the slight decline from November, indicating a cautious but hopeful recovery in workforce levels. Despite this, backlogs of work continued to deplete, which may suggest that companies are streamlining operations and addressing accumulated workloads. The reduction in backlogs, while typically a sign of improved efficiency, also reflects a slower pace of new orders to replace the work completed.

Read More: Japan Consumer Confidence

Input Prices and Costs Rise Amid Weak Yen

On the cost side, input prices rose at the sharpest rate since August 2024, driven by a weaker yen and higher costs for raw materials. The currency depreciation, in particular, placed upward pressure on import costs, exacerbating challenges faced by manufacturers who rely on imported goods and components. In response to rising costs, firms increased selling prices at the strongest rate seen in five months. While this price adjustment helps mitigate some of the financial pressures, it also risks impacting demand, particularly if consumers or businesses become less willing to pay higher prices in a slowing economic environment.

Meanwhile, buying activity remained subdued for the third consecutive month, as companies appeared to be cautious with their inventory purchases. The extended delivery times for inputs, though marginal, indicate that supply chain issues may still persist, affecting the timeliness of production schedules. This, in turn, could further complicate efforts to ramp up output or respond quickly to shifts in market demand.

Sentiment Shows Optimism for the Future

Despite the ongoing contraction in output, sentiment within the manufacturing sector was relatively optimistic. Firms expressed confidence, fueled by expectations for mass production of newly launched products in key industries. The semiconductor and automotive markets, in particular, were highlighted as areas of recovery, providing hope for a rebound in demand and output. Business expansion plans, along with the anticipation of future growth in these sectors, contributed to a more positive outlook.

This optimism is reflected in the business expectations sub-index, which remained resilient despite the ongoing challenges in production. Manufacturers appear to be cautiously optimistic about the future, particularly as they look to capitalize on emerging trends in technology and new product development. As such, while the sector continues to face headwinds, there is hope that the current contraction will be short-lived, with the potential for a recovery in the coming months, especially if global demand improves and supply chain issues ease.

Overall, while Japan’s manufacturing sector faces a challenging period, the recent data suggests that the pace of contraction is slowing, and there are reasons for cautious optimism moving forward. However, the path to full recovery remains uncertain and will depend largely on the global economic environment, domestic demand, and how well Japanese manufacturers can adapt to ongoing cost pressures and supply chain disruptions.

Share

Hot topics

What is News Trading in Forex? A Complete Guide to Event-Driven Strategy

Introduction If you have ever watched the forex market during a major economic announcement, you know how dramatic it can be. Prices jump within seconds. Spreads widen. Volatility explodes. For...

Read more

Submit comment

Your email address will not be published. Required fields are marked *