China’s Industrial Production Grows 6.1% in April 2025

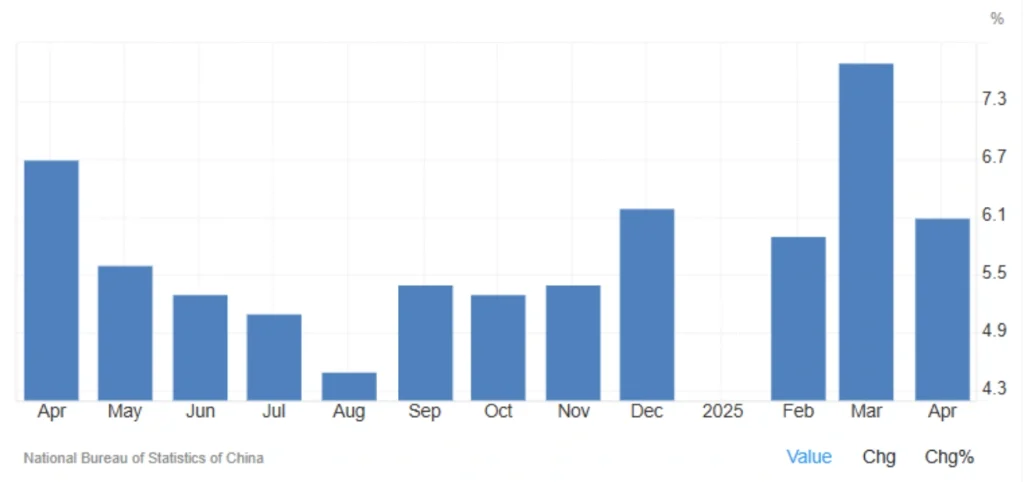

China’s industrial production rose by 6.1% year-over-year in April 2025, surpassing market expectations of 5.5%. However, this marks a slowdown from the 7.7% growth in March, which had been the strongest figure since June 2021. Growth across all major sectors continued, albeit at a more moderate pace.

Key Highlights – China Industrial Output, April 2025

| Sector | April YoY Growth | March Growth |

|---|---|---|

| Total Industrial Output | ▲ 6.1% | ▲ 7.7% |

| Manufacturing | ▲ 6.6% | ▲ 7.9% |

| Electricity, Gas, Water | ▲ 2.1% | ▲ 3.5% |

| Mining | ▲ 5.7% | ▲ 9.3% |

| Monthly Growth | ▲ 0.22% | – |

- 🔍 YTD Growth (Jan–Apr 2025): 6.4%

- 🔍 Full-year Growth in 2024: 5.8%

Educational Focus: What Is China’s Industrial Production Index & Why Does It Matter?

The Industrial Production Index measures the output of factories, mines, and utilities. For China, a global manufacturing hub, this metric serves as an early indicator of global economic health, given its vital role in the world’s supply chains.

🔍 Why It’s Crucial for Markets:

- Reflects global demand for raw materials

- Signals export performance and manufacturing trends

- Impacts global commodity prices (steel, aluminum, energy, etc.)

Interpretation: Economic Signals, Global Impact, and Policy Implications

Despite slowing from March’s surge, April’s 6.1% growth signals underlying stability in China’s industrial recovery, with a gentler momentum that may prove more sustainable.

Notably, 36 out of 41 major manufacturing sub-sectors posted growth, including:

- Computers & Communications: ▲ 10.8%

- Automobiles: ▲ 9.2%

- Chemicals: ▲ 8.0%

- Non-ferrous Metals: ▲ 7.5%

- Ferrous Metal Smelting: ▲ 5.8%

- Coal Mining: ▲ 6.3%

Factors Behind the Slower Growth Pace:

- Wind-down of pre-tariff production boost ahead of U.S. trade measures

- Weaker demand from key trading partners such as the U.S. and Europe

- Seasonal and internal fluctuations in energy and raw material consumption

April’s monthly growth of just 0.22% also points to a more cautious stance among industries, likely influenced by uncertainty around U.S. trade policy.

Read More: China’s Industrial Production Growth Surpasses Expectations in 2025

Summary: Opportunities vs. Risks

✅ Opportunities:

- Sustained, diversified growth across various industries

- Strengthening domestic industrial infrastructure

- Potential export expansion in technology, automotive, and chemicals

⚠️ Risks:

- Slower growth may suggest post-tariff saturation or strategic caution

- External demand pressures from Western economies

- Possible weakness in energy and mining if global commodity prices decline

Final Take

China’s April 2025 industrial output outperformed expectations, yet the cooling momentum hints at a more balanced and cautious industrial landscape. While the overall outlook remains positive, external risks—particularly trade policy uncertainty—pose notable challenges for the months ahead.

Share

Hot topics

What is Balance in Forex? A Complete Guide for Traders

Introduction When you open a trading account for the first time, one of the first numbers you see on your screen is your balance. It looks simple. It looks clear....

Read more

Submit comment

Your email address will not be published. Required fields are marked *