Australia’s Manufacturing PMI Climbs to Six-Month High

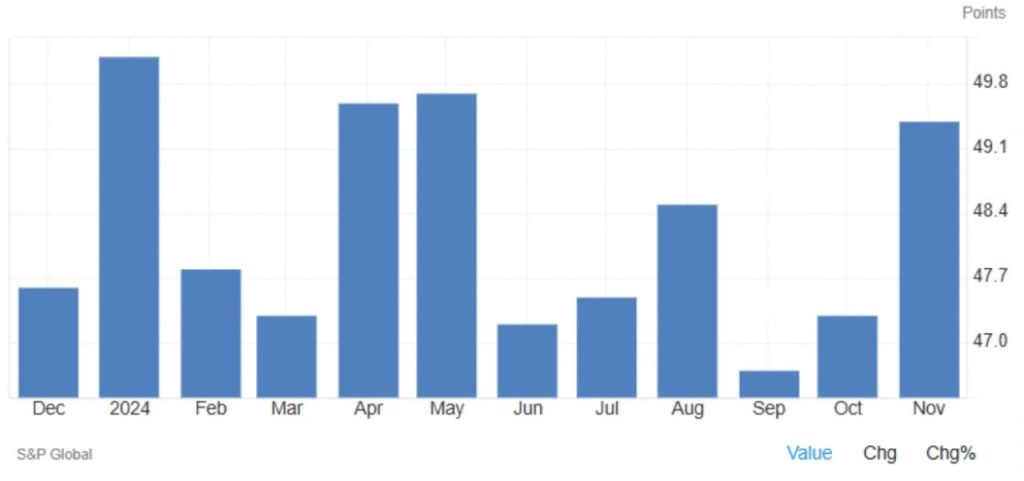

Australia’s manufacturing sector showed signs of recovery in November 2024, as the Judo Bank Manufacturing PMI rose to 49.4, the highest reading in six months, up from October’s 47.3. Although the index remained below the neutral 50-mark—indicating continued contraction—the slower rate of decline brings cautious optimism. Key drivers behind this improvement include easing contractions in production and new orders, including exports, which had faced significant pressure in recent months.

This rebound suggests that the worst of the downturn may be over, even as challenges linger. Manufacturers have demonstrated resilience, adjusting their strategies to cope with demand fluctuations and supply chain disruptions. While the sector isn’t out of the woods yet, the latest data provides a glimmer of hope for a turnaround in the coming months.

Business Sentiment Reaches New Heights

One of the most encouraging findings in November’s report was the surge in business confidence. Sentiment among manufacturers reached its highest level since January 2023, fueled by hopes of improved market conditions in the future. This wave of optimism had a tangible impact on employment, as businesses increased hiring for the first time in six months.

However, despite these gains, firms remain cautious. Subdued consumer demand and market uncertainties have prompted many manufacturers to streamline operations, reducing inventories and scaling back purchasing activities. This approach reflects a strategy of balancing optimism for recovery with the realities of current market conditions.

Persistent Supply Challenges Add Pressure

Supply chain issues continue to pose significant obstacles for Australian manufacturers. Delays stemming from congestion in the Red Sea and Asia have extended lead times, contributing to higher transportation and input costs. While these challenges persist, there was a notable easing in input cost inflation, which fell to its second-lowest rate since 2016.

Despite this relief, manufacturers are treading carefully. Selling price increases were modest, rising at the slowest rate since August 2020. This indicates that businesses are reluctant to pass on higher costs to consumers, likely in an effort to remain competitive in a market where demand remains fragile.

Stabilization Amid Cautious Optimism

The November PMI report paints a picture of a sector navigating between challenges and opportunities. While the manufacturing environment remains tough, signs of stabilization are becoming evident. Slower rates of contraction in key metrics, coupled with improved sentiment and employment growth, suggest the sector is finding its footing after a difficult period.

Moving forward, the interplay between domestic demand, global supply chain dynamics, and economic data—such as the upcoming U.S. labor market figures—will play a critical role in shaping the recovery trajectory. For now, cautious optimism prevails, with manufacturers bracing for a gradual but hopeful path to stability and growth.

Share

Hot topics

What is News Trading in Forex? A Complete Guide to Event-Driven Strategy

Introduction If you have ever watched the forex market during a major economic announcement, you know how dramatic it can be. Prices jump within seconds. Spreads widen. Volatility explodes. For...

Read more

Submit comment

Your email address will not be published. Required fields are marked *