week 12 begins under the shadow of oil and the Fed

The global economy enters Week 12 under a heavier macro cloud, with markets caught between slowing growth signals and a renewed inflation threat from the Middle East oil shock. Brent closed above $103 on Friday, the U.S. dollar stayed firm, and investors sharply reduced expectations for near-term Fed easing ahead of the March 17–18 FOMC meeting, where updated projections are likely to shape the global risk tone for the week. The result is a more fragile backdrop for equities and cyclical assets, while recession fears and stagflation risks are both moving higher again.

Global Economy Weekly Review

The global economy remained in expansion over the past week, but the tone became noticeably more fragile. The main message from the data was that growth is slowing across several major economies, inflation is no longer the central panic but remains sticky enough to restrict central banks, and the Iran-linked oil shock has revived both upside risks to prices and downside risks to activity.

The biggest global development was the sharp rise in oil prices early in the week, driven by fears of supply disruption through the Middle East and the Strait of Hormuz. Even though crude later pulled back from its highs, the shock was strong enough to reshape the macro narrative. It raised concerns about persistent energy-led inflation, weaker growth for importers, and renewed volatility across equities, bonds, currencies, and commodities.

In the United States, the economy looked cooler but still resilient. Q4 GDP was revised down sharply, confirming weaker late-2025 momentum, but jobless claims stayed low, GDPNow remained relatively solid, and spending still held up in nominal terms. Inflation looked more contained on the surface, though core measures stayed sticky, leaving the Fed cautious.

The United Kingdom and euro area looked softer. UK growth was flat, manufacturing and retail disappointed, and confidence weakened. In the eurozone, industrial weakness remained the main drag, especially in Germany and Italy, while inflation stayed moderate enough to avoid a fresh alarm.

China was one of the stronger stories, with firmer inflation, easing producer-price deflation, solid trade, and stronger credit data. Still, the recovery remains dependent on exports and policy support. Japan also improved, with stronger GDP, wages, and lending, though household demand stayed soft.

Across emerging markets, resilience became more selective. India and Brazil held up relatively well, while Turkey remained fragile and Mexico softened. Overall, the world economy is still growing, but with less margin for error, greater sensitivity to oil and geopolitics, and a more difficult policy backdrop.

U.S. Weekly Economic Review: Growth Cools, Inflation Stays Sticky, but Demand Has Not Broken

The U.S. economy sent a mixed but still broadly resilient signal over the past week. The main takeaway is that growth has slowed meaningfully from the stronger pace seen in late 2025, but the economy is not showing signs of broad weakness. Inflation is easing, though not fast enough to remove pressure from the Federal Reserve, while consumer demand and the labor market remain stable enough to keep recession fears contained.

The clearest sign of slowing came from the latest Q4 GDP revision, which showed the economy expanded at just 0.7% annualized, down from 1.4% previously and far below the prior quarter’s 4.4% pace. Real final sales and consumer spending were also revised lower, confirming that late-2025 momentum weakened more sharply than first estimated. Still, this softer backward-looking picture was partly offset by the Atlanta Fed GDPNow, which remained at 2.7% for Q1, suggesting activity at the start of 2026 has been firmer than the Q4 data alone imply.

Inflation data supported the view that disinflation is continuing, but slowly. February CPI and January PCE both showed headline inflation staying relatively moderate, but core inflation remained sticky, especially core PCE at 3.1% year-on-year. The Dallas Fed trimmed mean PCE also reinforced the idea that underlying inflation pressures are still above comfort levels. Treasury yields remained elevated, reflecting that markets still see inflation as persistent enough to keep the Fed cautious.

The consumer sector is holding up, but with more caution. Personal spending rose in nominal terms, though real consumption was only slightly positive, showing inflation is still absorbing part of household spending power. Sentiment data reflected that split: current conditions improved, but expectations weakened, indicating households feel okay about the present but remain uncertain about the future.

The labor market remains one of the strongest stabilizers. Jobless claims stayed low, continuing claims improved, and hiring remained modestly positive. That does not suggest a labor market in rapid deterioration. Housing data were also mixed but better than feared, with existing home sales and housing starts surprising to the upside, even as permits weakened.

Meanwhile, business investment and trade showed signs of moderation rather than contraction. Durable goods were soft on the headline, but core orders remained positive. The trade deficit narrowed sharply, offering some support to Q1 growth.

Overall, the U.S. economy looks like it is slowing, but not breaking. Growth has cooled, inflation is still sticky underneath, and the Fed is unlikely to pivot easily.

U.S. Economic Outlook: Week Ahead

The U.S. economy enters the week of March 16–21, 2026 in a more fragile position than markets expected just a few weeks ago. Growth has clearly slowed, inflation remains sticky, and the recent oil shock tied to Middle East tensions is making the Federal Reserve’s job more difficult. The main expectation is that the Fed will leave rates unchanged, but its tone may be firmer than markets would like because inflation risks are rising again just as activity softens.

The backdrop is uncomfortable. Q4 2025 GDP growth was revised down to 0.7% annualized, while February payrolls weakened and consumer sentiment deteriorated, with the University of Michigan index slipping to 55.5. At the same time, inflation has not fully eased. CPI remains above target, PCE inflation is still near 3%, and higher energy prices are adding fresh upside pressure. This creates a clear growth scare versus inflation scare dynamic for the week ahead.

That leaves a fairly straightforward base case. First, the Fed is expected to hold rates steady. Second, the updated SEP and dot plot are unlikely to signal aggressive near-term cuts. Third, Chair Powell will probably acknowledge weaker growth but stress inflation uncertainty and the need for data dependence. Markets are therefore likely to react as much to the tone and projections as to the policy decision itself.

On the data side, Industrial Production on Monday will be the main hard-activity release and will show whether manufacturing is stabilizing or weakening further. PPI on Wednesday matters because it will offer one more inflation signal just before the Fed decision. Retail sales and housing data remain important, though their release timing is still uncertain because of calendar disruptions following the 2025 government shutdown. Finally, jobless claims, new home sales, and the Philadelphia Fed survey on Thursday will help assess labor-market resilience, housing momentum, and factory conditions.

Overall, the week looks set to test whether the U.S. is merely slowing or moving toward a more stagflationary mix.

Event of the week: FOMC Meeting, March 17–18 Preview

The March 17–18 FOMC meeting is the central macro event of the week because it includes a new Summary of Economic Projections (SEP) as well as the updated dot plot. Markets still overwhelmingly expect the Fed to leave rates unchanged at 3.50%–3.75%, so the focus will not be on the rate decision itself, but on the message, projections, and Chair Powell’s assessment of the economic outlook.

The Fed enters the meeting facing a more difficult backdrop than in January. Growth has slowed, the labor market has softened, and inflation has not made enough progress back toward 2%. At the same time, the Iran-linked oil shock has pushed up energy prices, raising the risk that inflation stays sticky for longer even as growth cools. That combination has increased stagflation concerns and made the Fed’s dual mandate harder to manage.

The base case is a hawkish hold. The Fed is expected to acknowledge weaker growth and softer employment conditions, while avoiding any strong hint of near-term rate cuts because inflation risks have re-emerged. Recent labor-market data have been mixed, with a strong January jobs report followed by a much weaker February reading, leaving conditions softer but not collapsing. Inflation data tell a similar story: price pressures are no longer accelerating sharply, but PCE inflation remains near 3%, and the oil shock may lift headline inflation further.

The SEP is likely to tilt in a more stagflationary direction, with higher inflation forecasts, lower GDP projections, and slightly higher unemployment estimates. Even so, the median dot plot may remain unchanged, as the Fed may prefer to preserve flexibility amid elevated uncertainty.

Political pressure is also building, with President Trump again publicly demanding rate cuts, but the Fed is likely to resist. Ultimately, this meeting is mainly about Powell’s framing of the next phase. If the Fed lowers growth forecasts while nudging inflation projections higher, markets will likely read that as a renewed higher-for-longer signal, supportive for the U.S. dollar and Treasury yields, but less favorable for equities and other rate-sensitive assets.

USD and Wall Street

For the week ahead, the clearest fundamental bias remains a supported U.S. dollar and pressured Wall Street, unless markets get either a credible geopolitical de-escalation or an unexpectedly dovish Fed surprise. In simple terms, the current macro setup still favors hawkish hold plus elevated oil = stronger dollar and weaker equities, while a calmer oil backdrop and a more balanced Fed could allow the dollar to ease and stocks to stage a relief bounce.

Last week, that pattern was already visible. The U.S. dollar strengthened sharply, with the DXY rising 1.5% to 100.35, as investors shifted into haven assets and pushed expected Fed easing further into the future. At the same time, Wall Street lost ground, with the Dow down about 2.0%, the S&P 500 down 1.6%, and the Nasdaq down 1.3%. The S&P 500 has now posted three straight weekly declines and sits roughly 5% below its late-January record high.

The main driver was a more difficult macro mix. Oil prices rose back above $100, inflation concerns firmed, growth data weakened, and confidence in near-term Fed cuts faded. CPI and PCE data showed inflation moderating only slowly, while Q4 GDP was revised down to 0.7% and consumer sentiment slipped. That combination pushed markets toward a more cautious interpretation: slower growth, but not enough disinflation to justify easy Fed easing.

This week’s key event is the March 17–18 FOMC meeting, especially because it includes new projections and the dot plot. The base case is still no rate change, but the risk is that Powell emphasizes inflation risk more than slowing growth. That would reinforce the bullish-dollar view.

Technically, the USD Index still looks constructive. It remains in a rising channel and is testing the 100.25–100.50 resistance zone. The trend is bullish, though RSI near 73 suggests overbought conditions and raises the risk of short-term consolidation. A break above 100.50 would open room toward 101.00–101.50, while failure there could trigger a pullback toward 99.00.

For Wall Street, the outlook stays cautious and volatile. The Dow’s daily chart is bearish, with lower highs and lower lows since mid-February and price testing 46,500 support. RSI near 27 suggests oversold conditions, so a bounce is possible, but the broader structure remains weak unless the index reclaims 48,000–49,000.

Central Banks in Focus

It is going to be an important week for global central bank decisions as they can reflect divergent economic conditions. China’s PBOC is likely to maintain a “moderately loose” stance (holding policy tools like the 1-year loan prime rate at 3.0%) as growth cools and inflation remains near zero. Canada’s BoC (policy rate 2.25%) is expected to hold steady given a surprising Q4 GDP contraction (annualized –0.6%) and easing inflation (≈2.3% in Jan). Japan’s BOJ (yield cap ~0.75%) should also pause, despite strong wage gains and a modest rise in core Tokyo inflation (1.8% Feb), as markets largely price the next hike for mid-2026. Switzerland’s SNB (policy ~0%) will almost certainly stay put amid near-zero inflation (0.1% in Jan). The BoE (Bank Rate 3.75%) faces widespread market bets on a cut in March as UK CPI fell to 3.0%

while unemployment rose to ~5.2%. The ECB (refi 2.00%) is expected to hold, even though euro-area inflation may rise toward 2.0% by summer; focus will be on war-driven energy risks. Australia’s RBA (cash rate 3.85%, after Feb hike) is likely to pause on Mar 16–17. High recent inflation (3.6% Q4) and surprising growth (GDP +0.8% q/q) argue for caution. Key risks include energy shocks, trade tensions, and data surprises.

Gold market condition and weekly Outlook

Gold enters the new week in a near-term corrective phase rather than a fresh bullish breakout. Spot gold ended last week around $5,052/oz, down more than 2% and marking a second straight weekly decline. The key message is that gold is still benefiting from safe-haven demand linked to war risk, but that support is currently being outweighed by a stronger U.S. dollar, higher Treasury yields, and reduced expectations for near-term Fed easing.

The market regime has shifted. Gold is no longer trading mainly as a simple geopolitical hedge. Instead, it is caught between two competing forces. On one side, the Iran war, supply disruption fears, and broader macro uncertainty continue to provide an underlying floor for bullion. On the other, firmer U.S. yields, a stronger dollar, and the repricing of Fed cuts are limiting upside. This leaves gold looking short-term pressured but still medium-term constructive. Structural support remains in place through central-bank buying, ETF inflows, and broader asset-allocation demand.

The main event this week is the March 17–18 FOMC meeting. Markets expect no change in rates, but the tone of Chair Powell’s message, the updated forecasts, and the dot plot will matter far more for gold than the decision itself. The challenge for gold is that the macro mix is not especially favorable in the short run. U.S. growth has weakened, with Q4 GDP revised down to 0.7%, which would normally support gold through lower yields. But inflation remains sticky, with core PCE still around 3.1%, while the oil shock has added fresh upside inflation risk. That makes it harder for the Fed to sound confidently dovish.

Oil is another crucial factor. Brent above $103 and WTI near $99 highlight that energy prices are now feeding directly into the inflation narrative. For gold, that creates a split effect: geopolitical oil risk supports safe-haven demand, but higher oil also strengthens the dollar and yields, which act as headwinds. Last week, the negative side of that balance dominated. The dollar has effectively become the market’s preferred haven during the conflict, which explains why gold has not fully capitalized on geopolitical stress.

Technically, XAUUSD remains constructive in the medium term, but the short-term setup is neutral to slightly bearish. Price is consolidating around the 5,020 zone, momentum is neutral, and buying pressure has slowed. Above 5,000, gold can remain range-bound and attempt recovery. Below 5,000, the risk of a deeper correction toward 4,900 rises. A stronger bullish recovery would likely require a move back above 5,150–5,200.

Crude oil market condition and weekly outlook

Oil enters the new week in a supply-shock market rather than a normal demand-driven one, which keeps the near-term fundamental backdrop supportive but also makes price action highly sensitive to headlines. The core driver remains the disruption around the Strait of Hormuz, meaning crude can still swing sharply on any news about shipping, reserve releases, or diplomacy.

Last week, the energy market stayed strongly bid. Brent settled at $103.14 and WTI at $98.18 on Friday, after both benchmarks reached their highest levels since 2022 earlier in the week. On a weekly basis, Brent rose 11.27% and WTI gained 8%, confirming that a substantial geopolitical risk premium is still embedded in prices.

The main reason is the supply disruption linked to the Middle East conflict. According to the IEA, oil flows through Hormuz have dropped from roughly 20 mb/d before the war to a trickle, while Gulf producers have cut output by at least 10 mb/d as storage fills and export routes remain constrained. The IEA also expects global supply to fall by 8 mb/d in March, although some of that could be offset later by non-OPEC+ producers.

At the same time, the market is no longer trading purely on panic. It is also weighing how much of the disruption can be absorbed through emergency intervention. IEA member countries have agreed to release 400 million barrels of emergency oil, while the U.S. has announced an SPR release, with the first barrels expected to reach the market by the end of next week. That offers some short-term relief, but it does not remove the underlying chokepoint risk if Hormuz remains heavily impaired.

U.S. inventory data added a mixed signal. Crude stocks rose, but gasoline and distillate inventories fell, while product demand remained firm. That suggests domestic crude availability improved somewhat, but the broader refined-product balance is still tight. U.S. drilling activity also edged higher, showing producers are beginning to respond to stronger prices.

For this week, the base case is high volatility with an initial upside bias, because supply risk remains dominant. As long as Hormuz stays constrained and Gulf exports remain disrupted, pullbacks are likely to be treated as temporary. However, the market also looks vulnerable to a sharp reversal if there is a verified de-escalation signal.

Technically, WTI is still bullish but very stretched. Momentum remains strong, but with RSI deeply overbought, the market is increasingly exposed to profit-taking and sharp corrections. Above 98.5, upside can extend toward 106.5. Below 92.0, the risk of a deeper pullback toward 85.5 increases.

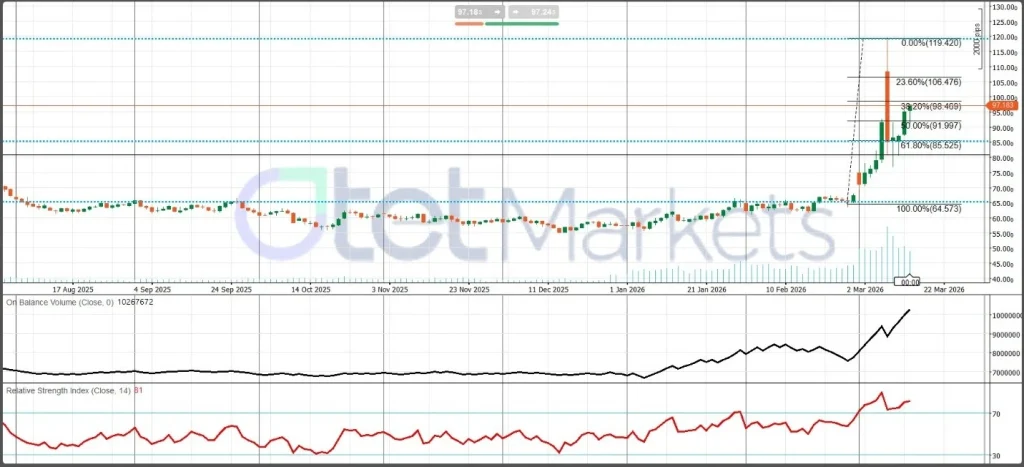

Crypto market condition and BTC weekly Outlook

Bitcoin enters the new week in a fragile recovery phase, not a clean new bull run. The broader crypto market has improved from the February panic, but BTC is still trading more like a macro-sensitive risk asset than a self-sustaining bullish market. That means short-term direction continues to depend less on crypto-specific optimism and more on the same forces driving equities and high-beta assets: the Federal Reserve, the U.S. dollar, Treasury yields, oil prices, and inflation expectations.

The medium-term backdrop is more constructive than price action alone suggests. Institutional demand has improved meaningfully. Digital-asset investment products saw strong weekly inflows, with Bitcoin accounting for the majority, while U.S. spot Bitcoin ETFs also recorded positive flows throughout the week. That tells us professional and long-term investors are still providing support underneath the market, even if short-term sentiment remains cautious. Regulatory developments in the United States also helped at the margin, with stronger coordination between the SEC and CFTC improving hopes for a more coherent oversight framework for crypto assets. That gave Bitcoin some support late in the week and helped it hold near a one-week high.

Still, the immediate macro environment is not especially favorable. Oil prices remain elevated, the U.S. dollar has strengthened, and Treasury yields have stayed firm as markets have pushed Fed-cut expectations further out. This is a difficult combination for Bitcoin because tighter financial conditions tend to reduce appetite for speculative or high-beta assets. In that sense, BTC is still behaving more like a macro risk trade than a defensive asset, even during geopolitical stress.

The key event this week is the March 17–18 FOMC meeting. For Bitcoin, the real issue is not just whether the Fed holds rates steady, but whether Powell sounds balanced or leans more firmly toward a higher-for-longer stance. A softer dollar, calmer oil prices, steadier yields, and a non-hawkish Fed hold would create the cleaner bullish setup for BTC. By contrast, a firmer dollar, higher oil, and a more inflation-focused Fed would likely keep Bitcoin capped and vulnerable to renewed selling.

Technically, BTC looks like a market trying to build a base after a breakdown. The daily structure has improved from outright bearish to neutral or mildly constructive, but it has not yet rebuilt a strong bullish trend. Momentum is neutral, and accumulation remains limited. As long as Bitcoin holds above 70,000, consolidation can continue with room for a recovery toward 75,000 and potentially 80,000. A break below 70,000 would increase downside pressure toward 65,000. Overall, BTC still looks like a cautious recovery inside a macro-driven market rather than the start of a fresh straight-line rally.

Share

Hot topics

What Is Liquidity in Trading Strategy?

Liquidity plays a role in price execution when trading. You may have noticed the price came in worse than you expected and have already experienced liquidity at work without realizing...

Read more

Submit comment

Your email address will not be published. Required fields are marked *