The Global Economy in March 2026: A Slower World, A Narrower Path

March 2026 begins with the global economy in a fragile but more balanced position: growth is slowing, inflation is easing, and central banks are moving closer to the next phase of policy decisions. In this global economic outlook, we examine the key trends shaping the month ahead—from the Fed, ECB, BoE, PBOC, and BOJ to inflation, labour markets, consumer demand, and global risk sentiment—and what they could mean for currencies, bond yields, equities, commodities, and broader market direction.

USA

The U.S. economy enters March 2026 with slower but still positive momentum, as easing inflation, a cooling labor market, and steady consumer demand keep the soft-landing narrative alive. This outlook examines the key macro themes shaping March, including Federal Reserve expectations, inflation risks, labor-market trends, and the major data releases that could drive the next move in yields, the dollar, and equities.

U.S. Economic Review – February 2026

In February 2026, the U.S. economy continued to shift into a late-cycle phase best described as cooling but resilient. Growth slowed from the stronger pace seen in late 2025, but the broader expansion remained intact. Consumer spending stayed supportive, while productivity gains linked to AI adoption and infrastructure investment helped offset some of the drag from softer exports, weaker public-sector momentum, and a more uncertain policy environment.

The clearest sign of moderation came from growth data. Real GDP rose at a 1.4% annualized pace in Q4 2025, down from 4.4% in Q3, showing that the economy was losing speed but not stalling. Even so, forward-looking estimates still pointed to above-trend activity entering February, supported by structural investment and efficiency gains across key sectors.

The labor market also showed a controlled slowdown rather than a sharp deterioration. Hiring cooled, with private-sector job creation remaining modest, but layoffs stayed low. Initial jobless claims held at 212,000, while continuing claims stood at 1.833 million, suggesting employers were slowing recruitment more than cutting staff. Wage pressures also eased, with labor-cost growth slowing to its weakest pace in several years. This combination pointed to a softer, but still relatively stable, employment backdrop.

Inflation continued to move lower, though not quickly enough to fully reassure policymakers. Headline CPI rose 0.2% month over month and 2.4% year over year, while core CPI increased 0.3% month over month and 2.5% year over year. Producer prices also remained firm, especially in services. The overall message was clear: disinflation was still progressing, but sticky underlying price pressures—particularly in shelter and services—kept the Federal Reserve cautious.

Consumer activity remained a key pillar of resilience. Retail data showed modest but positive gains, confirming that households were still spending despite slower overall momentum. At the same time, business investment signals were mixed. Headline durable goods orders weakened, largely due to transportation-related declines, but the core underlying trend was firmer, suggesting that private demand had not materially broken down.

The policy backdrop remained complicated. The Federal Reserve kept rates unchanged at 3.50%–3.75%, while FOMC minutes showed policymakers still divided between the possibility of later rate cuts and the need to stay alert to renewed inflation. Fiscal noise, a brief government shutdown episode, and geopolitical tensions added further uncertainty.

Overall, February reinforced the central theme of the U.S. economy in early 2026: slower growth, easing but sticky inflation, a cooling labor market, and continued resilience beneath the surface. The soft-landing narrative remains alive, but the path ahead is still narrow.

U.S. Economic Outlook – March 2026

The U.S. economy enters March 2026 in a more balanced but still fragile position. Growth is continuing, but at a slower and more sustainable pace than the stronger bursts seen in 2025. Inflation is easing, the labor market remains relatively firm, and consumers are still spending, but the economy is clearly moving deeper into a late-cycle phase where progress is becoming more uneven. For markets and policymakers alike, March is shaping up as a key month of confirmation: the question is no longer whether the economy is slowing, but whether it is slowing in a way that keeps the soft-landing narrative intact.

The baseline outlook remains constructive. Economic growth is expected to stay moderate through 2026, with expansion supported by steady household demand, improving productivity, and the ongoing contribution of AI-driven business investment. Manufacturing has shown signs of stabilization after earlier weakness, while services activity remains in expansion. This suggests that the economy still has forward momentum, even if businesses and households are behaving more cautiously than they did a year ago.

Inflation, meanwhile, continues to trend lower, but not fast enough to fully remove concern at the Federal Reserve. The broader disinflation story is still in place, yet underlying pressure in services, shelter, and wage-linked categories remains a challenge. That means March will be closely watched for signs that price pressures are either continuing to cool or becoming sticky again. If inflation softens further, confidence in a mid-year rate cut will increase. If not, expectations for higher rates for longer are likely to remain in place.

The labor market is another key pillar of the March outlook. Conditions are no longer as strong as they were during the peak of the post-tightening cycle, but they are still stable enough to support the broader economy. Hiring has slowed, wage growth is cooling, and businesses appear more selective, yet layoffs remain limited. This is an important distinction: the labor market is softening, not breaking. As long as unemployment remains contained and claims stay relatively low, the Fed can afford to be patient.

That is why the central policy expectation for March is unchanged: the Federal Reserve is widely expected to hold rates steady. Markets are focused less on whether the Fed will move immediately and more on how officials describe the road ahead. Any sign that the Fed is gaining confidence in the inflation trend would support expectations for easing later in 2026. A firmer inflation tone, however, would likely delay that timeline.

For investors, March is likely to be driven by incoming data rather than dramatic policy action. Bond yields may stay range-bound, equities could remain supported if disinflation continues, and the dollar may hold firm unless a clearer easing signal emerges. In short, March looks set to be a transition month—one that could either strengthen the case for a soft landing or remind markets that the path is still narrow.

UK

The UK enters March 2026 with modest growth, easing inflation, and a labour market that is cooling without breaking. This outlook explores what to watch from the Bank of England, fiscal policy, and the key economic trends shaping expectations for sterling, gilts, and UK equities as markets look for the first clear step toward lower interest rates.

UK Economic Review – February 2026

The UK economy moved through February 2026 with a familiar mix of weak growth, easing inflation, and a gradually cooling labour market. While the country avoided outright contraction, the month confirmed that the recovery remained fragile and uneven. Growth stayed positive, but only marginally, with services continuing to do most of the work while construction remained under pressure and manufacturing showed only limited resilience.

Official GDP data reinforced that picture. Real GDP rose just 0.1% month on month in December 2025, while output over the three months to December also increased by only 0.1%. This showed that the economy was still expanding, but at a very modest pace. Services output provided some support, but declines in production and construction highlighted how narrow the growth base remained. The broader message was clear: the UK economy was still moving forward, but without strong momentum.

The Bank of England’s February meeting became one of the month’s most important signals. The Bank kept Bank Rate unchanged at 3.75%, but the 5–4 vote split revealed that policymakers were moving closer to an easing cycle. With four members already voting for a cut, the decision suggested that the debate had shifted from whether rates would fall to when the first reduction would come. Markets interpreted the outcome as a sign that the BoE was leaning more clearly toward lower rates later in 2026.

Labour-market data also strengthened that view. Employment conditions softened further, with payrolled employment down by 121,000 over the year and the unemployment rate rising to 5.2%. Wage growth also moderated, with regular earnings slowing to 4.2% and private-sector pay growth easing further. Even so, vacancies remained relatively steady, suggesting the labour market was loosening gradually rather than breaking sharply. For policymakers, that is an important distinction: softer labour conditions reduce inflation pressure without necessarily creating a severe growth shock.

Inflation delivered the most encouraging development of the month. Headline CPI fell to 3.0% year on year from 3.4%, while core CPI eased to 3.1%. Lower transport and food prices helped drive the improvement, reinforcing the broader disinflation trend. However, services inflation remained above 4%, showing that domestic price pressures were still sticky and that the BoE could not yet move aggressively.

Consumer activity offered a mixed signal. Retail sales rebounded strongly, but confidence weakened, indicating that households remained cautious despite some short-term spending strength. Overall, February pointed to a UK economy edging closer to lower interest rates, but still constrained by weak growth, fragile confidence, and inflation that has not fully returned to target.

UK Economic Outlook – March 2026

The UK enters March 2026 in a delicate but manageable position. Growth is still positive, but only modestly, and the economy remains short of a broad, convincing recovery. Inflation has moved lower, the labour market is gradually cooling, and the Bank of England is now much closer to easing policy. That makes March an important month—not because the economy is about to accelerate, but because policymakers may be ready to begin adjusting to a softer inflation environment.

The main focus is the Bank of England. After holding rates at 3.75% in February with a narrow split vote, markets now see March as a live meeting. The Bank has signaled that inflation could move closer to its 2% target by spring, which has strengthened expectations for a possible 25-basis-point cut. Still, the decision is not guaranteed. Policymakers remain cautious because while headline inflation has fallen, domestic pressures—especially in services and wages—are still elevated enough to keep the debate open.

That is what defines the March outlook: the UK is moving toward lower rates, but not yet into a fully comfortable easing cycle. If inflation continues to soften and wage growth cools further, the case for a cut becomes much stronger. If services inflation stays sticky, the Bank may choose to wait a little longer. In other words, the direction is clear, but the timing still depends on incoming data.

Beyond monetary policy, fiscal policy also matters this month. The government’s early-March fiscal update could influence both growth expectations and the interest-rate path. Any looser fiscal stance—through tax relief or higher spending—could support activity in the short term, but it could also make the inflation outlook less straightforward. A tighter approach would likely reinforce the case for monetary easing by keeping demand more contained.

The growth backdrop remains soft. Consumer spending has shown some resilience, and industrial activity has improved in places, but confidence is still weak and the housing sector remains fragile. That suggests the UK is more likely heading into a slow-growth, low-momentum expansion than a sharp rebound. The labour market is also easing rather than collapsing, which is important. A gradual rise in slack gives the Bank of England more room to cut without immediately fearing a renewed inflation surge.

For markets, March is likely to be shaped by expectations around the Bank. A dovish signal would probably push gilt yields lower, keep pressure on sterling, and support equities. A more cautious tone could keep financial conditions tighter for longer. Overall, March looks like a transition month—one that could confirm the path toward lower rates, but only if inflation and wages continue to cooperate.

EU

The euro area enters March 2026 with modest growth, easing inflation, and an ECB that remains cautious as it balances slow expansion against still-fragile confidence. This outlook explores the key forces shaping the eurozone this month, including monetary policy expectations, inflation trends, domestic demand, and what they could mean for the euro, bond yields, and European equities.

Euro Area Economic Review – February 2026

The euro area moved through February 2026 with a cautiously improving economic backdrop. Growth remained modest, inflation continued to ease, and manufacturing showed early signs of stabilisation, helping the region start the year on slightly firmer footing. However, the recovery was still uneven, with consumer confidence subdued, retail activity softer after the holiday period, and external demand continuing to weigh on trade and industry.

One of the most encouraging developments was the further decline in inflation. Headline euro-area inflation fell to 1.7% year on year in January, down from 2.0% in December, bringing it closer to the European Central Bank’s target. Core inflation also eased to 2.2%, its lowest level since late 2021. Energy prices remained a major disinflationary force, while food inflation also moderated. Even so, services inflation stayed relatively elevated, showing that domestic price pressures had not fully disappeared.

That helped explain the ECB’s cautious stance in February. At its early-month meeting, the central bank left interest rates unchanged, keeping the deposit rate at 2.00%. Policymakers signaled that inflation was moving in the right direction, but they were not ready to declare victory. The message from Frankfurt remained clear: policy is now in a comfortable holding phase, and any future move will depend on incoming data rather than a preset path.

Growth data also pointed to resilience, but not strength. The second estimate for Q4 2025 GDP confirmed that the euro area expanded by 0.3% quarter on quarter and 1.3% year on year. Consumption and investment were the main drivers, while net exports remained a drag. This highlighted an important theme for the region: domestic demand is supporting growth, while weaker external conditions continue to limit momentum.

The manufacturing picture improved during the month. Survey data showed the sector moving from contraction toward expansion, with February flash PMI readings indicating that factory activity had returned to growth. Germany played a major role in that rebound, while services activity also remained steady. Still, industrial production and trade data suggested the sector was stabilising from a weak base rather than entering a strong recovery.

Overall, February confirmed that the euro area economy is improving gradually. Inflation is moving lower, growth remains positive, and industry is no longer deteriorating as sharply as before. But the recovery is still fragile, and the ECB’s cautious approach reflects an economy that is healing slowly rather than accelerating.

EU Economic Outlook – March 2026

The euro area enters March 2026 in a steadier position than it occupied a year ago, but the expansion remains slow and vulnerable. Growth is still positive, inflation is easing, and the labour market continues to provide support, yet the region is not moving into a strong recovery. Instead, the most likely near-term path is a low-speed expansion led by domestic demand, while trade, confidence, and parts of industry remain softer. ECB staff projections still point to modest growth in 2026, with fiscal deficits and public debt drifting higher over the medium term, which means the macro backdrop is improving, but not without constraints.

The main event in March is the European Central Bank. After leaving rates unchanged in February, the ECB is widely expected to hold again at its 18–19 March meeting. The deposit facility remains at 2.00%, and recent comments from Christine Lagarde suggest policymakers still see current settings as appropriate while they wait for clearer evidence that inflation is fully settling back to target. In that sense, March is unlikely to deliver a policy shift. It is more likely to reinforce the ECB’s current message: inflation is improving, but the bank is still in no rush to ease.

That makes incoming data especially important. Early March inflation figures, followed by labour, retail, industrial, and PMI releases later in the month, will shape how markets think about the path beyond spring. If inflation continues to soften while activity remains weak but positive, investors are likely to lean more confidently toward eventual easing later in the cycle. If, however, services inflation or wage-linked pressures remain sticky, the ECB may maintain a restrictive bias for longer than markets would like. The key issue is no longer headline disinflation alone, but whether underlying domestic inflation is cooling enough to justify a future policy pivot.

For markets, the likely March setup is relatively clear. A softer inflation trend and subdued growth would be supportive for euro-area bonds and equities, while putting mild downward pressure on the euro. A firmer growth or inflation surprise would likely keep yields higher and strengthen the case for a longer ECB pause. Overall, March looks like a confirmation month for the euro area: the region is stabilising, but the recovery is still narrow, cautious, and highly dependent on incoming data.

China

China enters March 2026 with growth still intact, but the recovery remains uneven as weak domestic demand, subdued inflation, and continued property-sector pressure keep momentum fragile. This outlook examines the key themes shaping China’s economy this month, including PBOC policy, credit conditions, consumption trends, and what they could mean for the yuan, Chinese bonds, and equity markets.

China Economic Review – February 2026

China’s economy moved through February 2026 with a familiar pattern: growth remained positive, but momentum stayed soft and uneven. Services continued to outperform, manufacturing held only slightly above the expansion line, and policymakers relied on targeted support rather than broad stimulus. The overall message from the month was clear—China is stabilising, but it is not yet entering a strong or broad-based recovery.

Business surveys showed that activity was still expanding, though only modestly. The Caixin Manufacturing PMI rose to 50.3, keeping factory activity just above the threshold that separates growth from contraction. Meanwhile, the services PMI improved to 52.3, confirming that services remained the stronger part of the economy. Together, these readings suggested that domestic activity was holding up, but not accelerating. Services were doing most of the work, while industrial momentum remained fragile and still lacked the strength needed to support a wider rebound in investment, hiring, and pricing power.

Inflation data reinforced the picture of weak domestic demand. Consumer prices rose just 0.2% month on month and 0.2% year on year, showing that household spending remained cautious and that inflationary pressure was still minimal. At the producer level, PPI stayed in deflation at -1.4% year on year, although that was an improvement from the previous -1.9%. This suggested that upstream price weakness had eased slightly, but not enough to signal meaningful reflation. In short, inflation remained too low to indicate strong demand recovery.

The property sector continued to be the biggest drag on confidence. House prices fell 3.1% year on year, a deeper decline than previously, confirming that the housing downturn was still worsening rather than stabilising. That mattered not only for real estate itself, but also for household wealth, local government revenues, and the broader willingness of firms and consumers to borrow and spend.

Credit data showed that liquidity support was still being provided, but demand for traditional borrowing remained selective. New loans missed expectations, while broader financing measures were stronger, suggesting policymakers were supporting the system through wider channels even as private-sector borrowing appetite stayed soft. This pointed to an economy where credit supply was available, but confidence was not strong enough to translate that support into stronger demand.

Overall, February confirmed that China’s recovery remains two-speed: services and selective external sectors are supporting growth, while weak inflation, fragile sentiment, and a deep property downturn continue to hold the broader economy back. Policy support remains measured and targeted, which should help maintain stability, but for now, the recovery is still gradual rather than decisive.

China Economic Outlook – March 2026

China enters March 2026 with growth still intact, but the recovery remains uneven and heavily dependent on policy support. The economy met its 2025 growth target of 5.0%, yet that headline result was driven more by exports and industrial activity than by a strong domestic rebound. Household demand remains soft, the property sector is still under pressure, and inflation is too weak to suggest a convincing improvement in underlying demand.

That makes March a month of cautious stability rather than acceleration. The core issue is not whether China is growing, but whether that growth can remain steady without broader stimulus.

Domestic demand remains the main weak point. Retail sales growth in 2025 was only 3.7%, well below pre-pandemic norms, showing that consumers are still spending carefully. Household confidence continues to be weighed down by flat income growth and ongoing weakness in housing. At the same time, the economy’s composition remains unbalanced: industry and exports are doing more of the work, while services and consumption are not yet strong enough to create a healthier, more self-sustaining expansion.

Inflation trends reinforce that picture. Consumer inflation is still near zero, while producer prices remain weak, highlighting the absence of strong pricing power in the economy. Imported inflation is also subdued, helped by lower global commodity, grain, and energy prices. This gives the People’s Bank of China room to remain accommodative. With inflation low and domestic demand fragile, policymakers are under no immediate pressure to tighten.

Monetary policy is therefore likely to stay supportive, but gradual. The PBOC kept the 1-year Loan Prime Rate at 3.00% and the 5-year LPR at 3.50%, while leaving the door open to further reserve requirement cuts or targeted easing later in the year. Liquidity is already ample, with M2 money supply up 9.0% year on year, but loan demand remains soft. That means the challenge is less about the availability of credit and more about weak confidence and limited appetite to borrow.

For markets, this leaves a familiar setup. Slower growth and subdued inflation should keep bond yields relatively low, while the yuan is likely to remain stable but capped by policy caution and soft domestic momentum. Chinese equities may struggle to build lasting upside unless policymakers deliver stronger fiscal support or consumption improves more clearly.

Overall, March 2026 looks set to bring steady but fragile growth, gradual policy easing, and continued focus on stabilising demand rather than pursuing aggressive stimulus.

Japan

Japan enters March 2026 with slow but positive growth, cooling inflation, and a Bank of Japan navigating a delicate balance between policy normalization and fragile domestic demand. This outlook explores the key macro themes shaping Japan this month, including wage trends, inflation risks, consumer weakness, and what they could mean for the yen, JGB yields, and Japanese equities.

Japan Economic Review – February 2026

Japan’s economy remained in expansion through February 2026, but the month highlighted a clear imbalance in where that strength is coming from. Business activity, exports, and corporate investment continued to show resilience, while household demand and consumer confidence remained much less convincing. The result was an economy that is still moving forward, but not yet with the broad-based momentum needed for a fully comfortable policy normalization.

The strongest signal came from private-sector activity. Both manufacturing and services stayed in expansion, with services once again leading the way. Survey data showed steady business momentum at the start of the year, while later flash readings suggested that activity strengthened further as February progressed. Manufacturing also improved, pointing to a more stable industrial backdrop than in previous months. This suggests Japan’s recovery is still intact, with service-sector demand and improving factory conditions helping support first-quarter growth.

However, the household picture remained softer. December household spending fell sharply, showing that consumer demand was fragile at the turn of the year. Retail indicators improved later, with January sales posting more encouraging gains, but the rebound was not strong enough to fully change the broader story. Consumers appear cautious, not confident, and that remains one of the main constraints on a stronger domestic recovery.

GDP data reinforced this view of modest underlying momentum. Japan’s fourth-quarter growth came in only slightly positive, with private consumption and capital expenditure both rising only marginally. At the same time, inflation-related measures within the GDP data remained elevated, highlighting a familiar problem: nominal activity is improving more clearly than real growth. In simple terms, Japan is still expanding, but not rapidly.

Corporate and external-sector data were more supportive. Machinery orders and machine tool orders rose strongly, indicating healthier business investment intentions and a firmer capex cycle. The external sector also remained a bright spot. A larger current account surplus, stronger exports, and a narrower trade gap showed that overseas demand was doing more of the work in supporting the economy. This helped offset weaker domestic demand and also supported the yen during the month.

Inflation cooled somewhat, but not enough to end the policy debate. Headline and core CPI eased, yet services inflation and producer-side price pressures remained firm enough to keep the normalization discussion alive. Wage growth, meanwhile, softened and confidence readings stayed subdued, underscoring that Japan has not yet secured a fully self-sustaining, wage-led expansion.

Overall, February confirmed that Japan’s economy is still growing, but the recovery remains uneven. Businesses and exporters are holding up well, while consumers remain the weak link. That leaves the outlook dependent on wages, household demand, and whether the Bank of Japan can continue navigating normalization without unsettling markets.

Japan Economic Outlook – March 2026

Japan enters March 2026 with the economy still growing, but only gradually and with an increasingly uneven mix of strengths and weaknesses. Growth has returned, but only marginally, and the recovery remains fragile. Business activity has been more resilient than household demand, inflation has cooled but not disappeared, and the Bank of Japan is now facing a more delicate policy balancing act than at any point in the past year.

The core issue for March is whether Japan can maintain slow expansion while moving carefully through the next phase of monetary normalization. Real GDP growth remains weak, and household demand is still the softest part of the picture. Consumer spending has not fully recovered, largely because real wages remain under pressure even as nominal earnings rise. That means households are still feeling the squeeze from living costs, which limits the strength of domestic demand and makes the recovery less durable than headline indicators might suggest.

At the same time, the broader economy is not stalling. Business surveys remain relatively constructive, and corporate sentiment is more resilient than consumer sentiment. Capital spending intentions have also been firmer than household activity, suggesting that companies are still willing to invest despite slower domestic momentum. This gives Japan a modest but important source of support going into the first quarter.

Inflation remains a key factor in the March outlook. Headline inflation has cooled, and some price pressures linked to imported costs have eased. However, underlying domestic inflation—especially in services—has remained more persistent. That leaves the Bank of Japan in a complicated position. Inflation is no longer running hot enough to force immediate action, but it is still firm enough in some areas to keep the discussion around further policy normalization alive.

This is why March matters so much for markets. The Bank of Japan is widely expected to hold rates, but investors will focus closely on its tone, especially around wages and the outlook for domestic inflation. If spring wage negotiations point to stronger pay growth, expectations for future tightening could rise again. If wage momentum disappoints and household demand stays weak, the case for a longer pause becomes stronger.

For markets, the most likely scenario is continued caution. Bond yields may remain sensitive to any shift in BOJ language, while the yen is likely to react to even small changes in rate expectations. Equities could remain supported by business resilience, but a weaker consumer backdrop may limit upside.

Overall, March looks like a transition month for Japan: slow growth, cautious policy, and a recovery that still depends heavily on whether wages can finally support stronger domestic demand.

Share

Hot topics

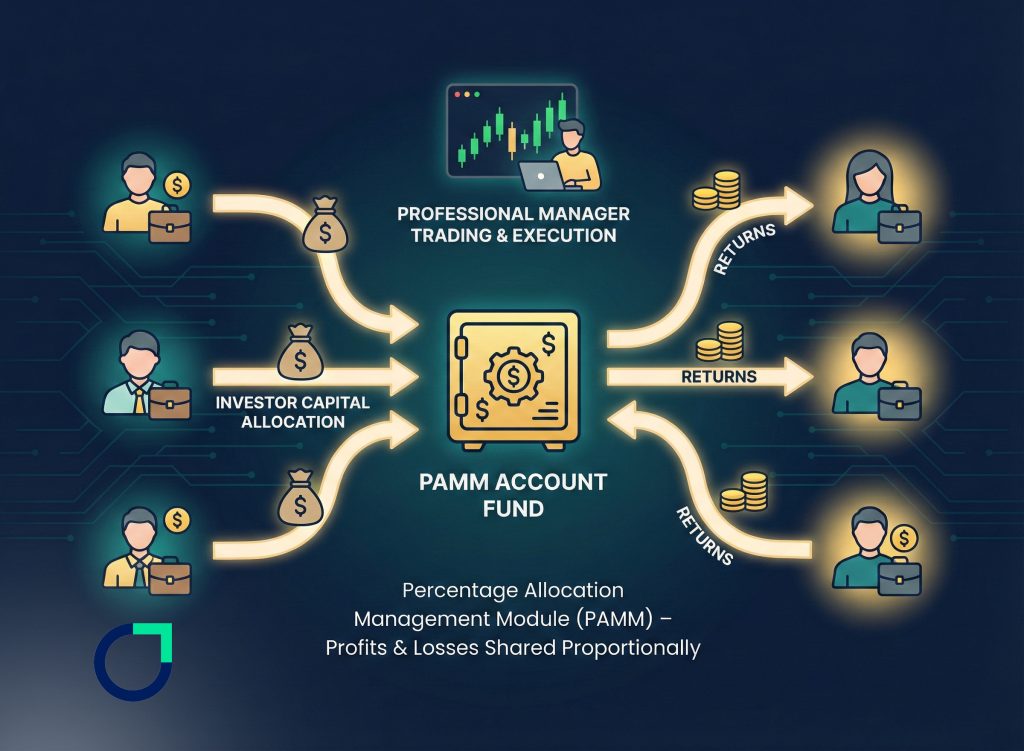

What Is a Forex PAMM Account? Complete Guide

Introduction If you’ve ever wanted to invest in Forex but had reservations about doing it alone, you’re not by yourself! Many people are interested in investing in the Forex market...

Read more

Submit comment

Your email address will not be published. Required fields are marked *