Otet View on Saturday, May 4, 2024

Labor market data in the US confirms that the Federal Open Market Committee (FOMC) will maintain its current policies and interest rates in the coming months. Following the FOMC meeting last week, Federal Reserve Chair Jerome Powell dismissed the possibility of an interest rate hike in 2024. However, he did not specify a date for a rate cut. Notably, the Non-Farm Payrolls (NFP) report released on Friday revealed that only 175 new jobs were created in April. This figure fell significantly below market expectations, reinforcing the cautious outlook of the Fed.

On the international front, there has been better-than-expected GDP growth in the European Union (EU). Additionally, inflation in the EU is showing signs of decreasing. These positive developments have sparked renewed hope for the Union economy.

Wall Street Overview:

As mentioned earlier, during its recent meeting, the Federal Open Market Committee (FOMC) decided to keep the target range for the federal funds rate unchanged at 5.25%-5.50%. The press conference and committee statement did not indicate any urgency to cut rates. Despite weaker-than-expected Non-Farm Payrolls (NFP) numbers at the start of the second quarter, the US unemployment rate remains at 3.9%, with a participation rate of 62.7%. This resilience suggests that the US economy can withstand the impact of high-interest rates.

Slower growth in the labor market, particularly with only a 0.2% monthly increase in average earnings, has led to eased Treasury yields. Nevertheless, the corporate bond market continues to signal optimism about future economic growth. In the upcoming week, we have more financial data to release, including consumer credit on Tuesday and consumer sentiment on Friday, which will provide further insights into the state of the US economy.

Last week’s data was positive for US stock markets:

- The S&P 500 recovered from Tuesday’s decline, closing approximately 0.5% higher.

- The Dow Jones Industrial Average increased by 1.1%.

- The Nasdaq Composite gained 0.9%.

Earnings reports also play a crucial role. Currently, more than 77% of S&P 500 companies have beaten estimates. 77% reported actual earnings per share (EPS) above expectations—above the 10-year average of 74%.

While less than 20% of S&P 500 companies are yet to release their earnings reports, we expect a quieter week ahead. The overall soft downward trend will likely persist unless Fed speakers’ surprises alter the outlook.

From a technical perspective, the US500 chart shows an overall downtrend. Key support levels include 5,000 and 4,900 (S1 and S2). However, reaching above 5,220 could potentially change the market trend, with the all-time high as the new target.

Forex:

For the currency market, we will have a busy week with the RBA Policy Rate (Tues.), Riksbank Policy Rate (Wed.), Bank of England Policy Rate (Thu.), BCB Policy Rate (Thu.), and Banxico Policy Rate (Thu.). Last week, the Fed held rates, and with a less hawkish outlook, it caused some pressure on the US dollar index.

Market estimates suggest that central banks in Australia and England will leave policy rates unchanged at 4.35% and 5.25%, respectively. On Thursday in Brazil also, we expect BCB to keep interest rates unchanged at 10.75% after six consecutive reduction seasons, as inflation has shown stubbornness in the reduction process in recent months. However, Banxico is the only central bank to continue reducing rates by another 25 basis points for the second consecutive season after eight months of holding rates unchanged.

The yen fell to a 34-year low last week, prompting possible BoJ intervention. With Japan’s Ministry of Finance and Central Bank (BoJ) supporting the beleaguered currency, JPY could recover quickly, which is expected to continue this week as well.

In the UK, with expected relative growth in GDP and the BoE holding rates, we do not expect a significant change in the GBPUSD trend. Sideways movement between 1.25 and 1.2560 is more realistic.

In Europe, economic data were a bit stronger than expected last week. For the week ahead, while the economic calendar is quiet in both the US and EU, we expect the soft upward trend to continue in the EURUSD chart, with 1.0867, 1.0980, and 1.1100 as the first, second, and third resistance levels ahead. On the flip side, if the pairing falls under 1.060, the downtrend can continue further with the next support at 1.050.

Commodity and Energy Market:

As tensions in the Middle East eased and US Treasury yields increased on most days of last week, gold lost some of its interest and demand, closing the week about 1.5% lower. However, for the next week, the scenario could change due to slowing bond yields, the relative weakness of the dollar, and the calming of the positive atmosphere caused by earnings reports in the stock markets during the last few weeks. Gold is expected to regain its safe-haven demand and begin to recover the levels lost over the past two weeks.

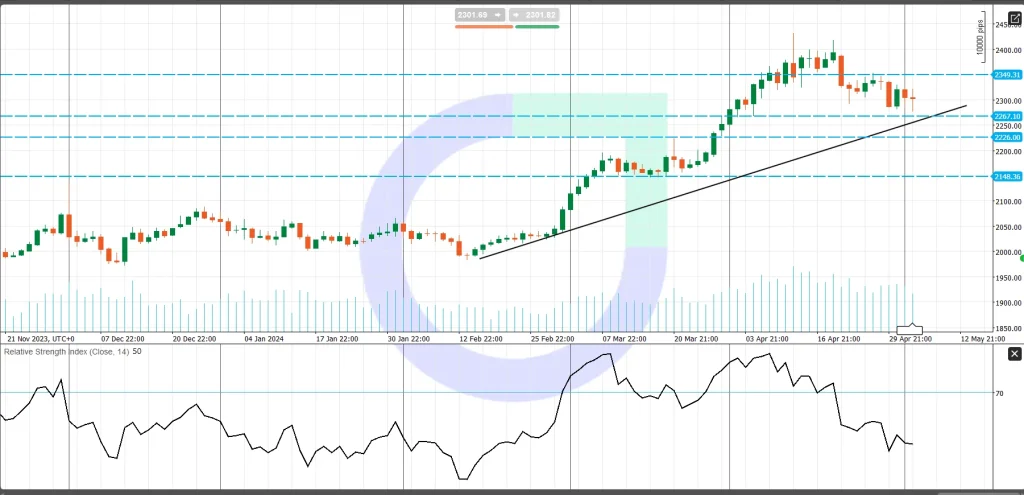

From a technical standpoint, in the daily chart, the price is still moving above the overall trend line. As long as the price remains above $2,267 US dollars, the bullish outlook remains unchanged, with $2,350 as the first resistance. Breaking above that could push the bulls toward the $2,400 area. On the flip side, falling below $2,226 could bring lower levels around $2,150 into focus.

Due to reductions in tensions, weaker-than-expected Chinese economic data, and a sharp increase in US petroleum inventories, WTI prices have been under pressure for the last two weeks. In the week ahead, attention will be focused on the EIA Short-Term Energy Outlook on Tuesday and Chinese inflation numbers on Saturday.

However, conflicts and tensions persist in Ukraine and the Middle East, suggesting that peace may not be imminent, especially with reports of Ukrainians targeting Russian refineries and Netanyahu’s intention to attack Rafah if peace talks remain incomplete.

Additionally, according to US Baker Hughes data, the Oil Rig Count fell to 499 last week, with the total Rig Count decreasing to 605 from the previous week’s 613. These numbers and data suggest that the downtrend may be ending, and a recovery could be expected next week. The initial target for WTI is $79.60, with further potential towards $84. From a technical standpoint, strong support lies at $76. If this level is breached and the daily candle closes below it, bears may re-enter the market, targeting $74.

Cryptocurrency:

The calm that settled in the market after the halving added pressure on prices, as the effects had already been priced in before the event. Even the introduction of Hong Kong spot Bitcoin and Ether exchange-traded funds (ETFs) failed to change the overall market sentiment.

Recently, Hong Kong launched spot Bitcoin and Ether exchange-traded funds (ETFs) after the Hong Kong Securities and Futures Commission (SFC) conditionally approved the issuance of spot BTC and ETH ETFs. At least three local issuers, including China Asset Management (ChinaAMC), Harvest Global, and Bosera International, have received the green light to launch these ETFs.

However, despite these developments, they have not been able to influence the ongoing price reduction. With a strong pivot at $67,000, bears are currently leading the price. The first and crucial support level is at $62,000, and if the weekly candle closes below that on Sunday, the next targets would be $59,000 and then $52,000. This scenario could change if the price moves above $67,000.

Share

Hot topics

What is Forex Rebate

Introduction If you have been trading Forex for a while, you have probably noticed that every trade comes with a cost. Whether it is spread, commission, or both, trading is...

Read more

Submit comment

Your email address will not be published. Required fields are marked *