Otet View on Saturday, May 18, 2024

Economic data this week confirmed that, despite a decrease in inflation, the Consumer Price Index (CPI) remains high at 3.4%, significantly above the Federal Reserve’s 2% target. Additionally, U.S. retail sales have started to show weakness, as indicated by the Leading Economic Index (LEI) on Friday.

Outside the U.S., the UK experienced wage growth; however, unemployment also increased to 4.3%. In Japan, GDP data surprised markets with a contraction of 2.0% annualized in Q1 2024. In China, there has been some progress in economic activities with industrial output firming and a gradual increase in inflation from negative digits, though retail sales have softened.

Looking ahead to next week, key economic events include:

- United States: Existing Home Sales (Wednesday), New Home Sales (Thursday), and Durable Goods Orders (Friday).

- Canada: CPI (Tuesday).

- United Kingdom: CPI, PMIs, and Retail Sales (Wednesday, Thursday, and Friday).

- China: PBoC Loan Prime Rate (Monday).

- New Zealand: RBNZ Interest Rate Decision (Wednesday).

- Turkey: CBRT One-Week Repo Rate (Thursday).

- Japan: Inflation data (Friday).

Wall Street

Long-term stubborn inflation and higher interest rates are showing their effects, as evidenced by the lack of growth in U.S. retail sales last month, while consumer credit increased monthly and savings declined. Consumer expectations and the new orders component of the ISM manufacturing index led to the Leading Economic Index (LEI) decreasing by 0.3 percentage points (pp) in April, bringing it to -0.6%. Despite these mixed economic signals, the labor market remains resilient, and income growth persists, potentially confusing FOMC members and consumers. As market participants harbor more doubts about the timing and extent of monetary policy easing, we can expect the LEI to continue its decline in the coming months.

Last week, market participants mainly focused on U.S. inflation numbers. The Producer Price Index (PPI) revealed a 0.5% increase in both headline and Core PPI for April, while March’s 0.2% increase was revised down to -0.1%. On the consumer front, inflation figures were somewhat optimistic, yet the 3.4% CPI remains well above the Fed’s 2% target. Optimistic inflation numbers initially supported U.S. stock markets and pressured the U.S. dollar, but when Fed speakers indicated the need for more evidence to justify reducing the inflation rate, bullish momentum paused.

Durable Goods Orders on Friday will be a key data point to watch in the week ahead. Economic and growth uncertainty continues to create an unfavorable environment for new capital investment. Durable goods orders increased by only 0.9% in March, and another weak growth of 0.5% is expected for April. Excluding transportation, durable goods orders have been essentially unchanged in recent months, which could raise concerns about future economic development.

Another important factor to monitor is the housing market. Higher interest rates are discouraging new construction and eroding affordability. Housing starts rose by 5.7% in April, primarily due to new multifamily developments, although the broader trend remains downward.

In the week ahead, we have Existing and New Home Sales data on Wednesday and Thursday. Although the housing market is far from its usual conditions, a rate cut outlook in September could moderate home price appreciation and attract buyers back. The market expects existing home sales to increase by 1.7% to a 4.19 million-unit pace in April.

Market participants are looking for more improvement in the housing market as monetary policy easing spurs a gradual retreat in mortgage rates. However, the 30-year fixed mortgage rate per Freddie Mac peaked at 7.2% in April, surpassing 7.0% for the first time this year, which could slow down builders. For April, we expect 680K new home sales, down from 693K in March.

Given the expected general weakness in the data, the high inflation, and the unchanged interest rates in the short term, we can anticipate a modest decline in most Wall Street indexes and stocks this week.

To print new record highs, the S&P 500 closed the week 1.6% higher, the Dow Jones gained 1.3%, and the Nasdaq Composite Index rose by 2.2%. For the week ahead, we will have a significant amount of data to watch. Some of these data points are crucial and can reveal the underlying trends in the economy.

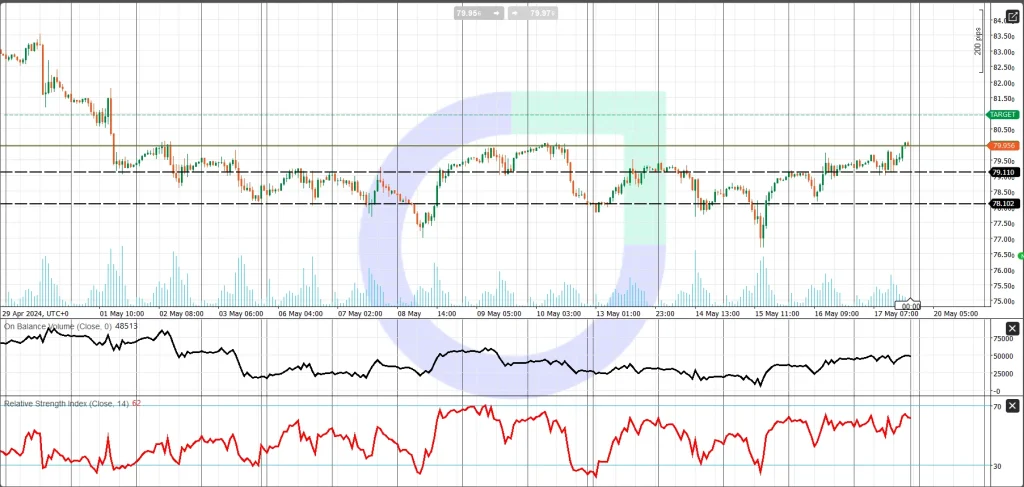

From a technical perspective, both On-Balance-Volume (OBV) and price are softening, while the Relative Strength Index (RSI) is retreating from above the 70 overbought areas, signaling a possible downturn. Falling below the previous high of 5,277 could set 5,223 and 5,150 as the targets for the week.

Forex Market in the Week Ahead

The U.S. Dollar Index (DXY) closed 0.8% lower this week. After falling in the first half of the week, the DXY attempted to recover some of its losses on Thursday and Friday, and this recovery is expected to continue in the upcoming week. On the H1 chart, market volume is increasing following the recovery, and the RSI is also rising towards the 50 level. If the RSI moves above 45 and 50 and the price rises above 104.60, we can expect the DXY to reach the 105 area in the week ahead. Conversely, a soft moving range between 104 and 104.60 is expected if the price cannot hold above 104.60.

In the UK, last week’s data confirmed wage growth, but the underlying details were less encouraging, with the unemployment rate rising to 4.3% and labor productivity falling by 0.3%.

In the week ahead, the focus will be on inflation numbers. CPI is expected to be 2.1% in April, with Core CPI projected to increase by 3.7%, both lower than March’s figures. Additionally, the market expects retail sales to decline by 0.2% in April. This could increase the likelihood of a Bank of England rate cut in August, potentially putting pressure on Sterling against its crosses.

From a technical point of view, on the H1 chart and in the short term, GBP/USD remains bullish and closed the week higher, mainly due to the weaker U.S. Dollar Index. The 61.8% Fibonacci fan at 1.2566 is the key support level for now, while the pivot point is set at 1.2500. S1 and S2 are positioned at 1.2610 and 1.2583, respectively. Holding above 61.8% of Fibonacci fans can support the bulls.

The Eurozone had a busy week, with no surprises. Inflation numbers for most EZ members were in line with estimates, showing more evidence of a gradual decline. Meanwhile, economic indicators such as GDP and industrial production confirmed the slow recovery. In the week ahead, the key market-moving data in Europe include German PPI (Monday), Eurozone trade data, and the ECB president’s speech on Tuesday. This light week with optimistic expected data can help the Euro hold its gains against its crosses.

From a technical point of view, the chart still depicts a soft uptrend, maintaining a positive outlook for the euro.

Commodity Market Outlook

In the commodity markets, precious metals, particularly Gold and Silver, continue to demonstrate potential for further increases, consistent with previous outlooks and analyses.

The recent weakness in the USD and the softer outlook for 2024 have contributed to the bullish sentiment in the gold market, which remains buoyed by its safe-haven demand. As economic and geopolitical risks intensify by the day, an increasing number of central banks, including the People’s Bank of China (PBoC) and the Central Bank of the Republic of Turkey (CBRT), are expressing interest in acquiring gold. The PBoC, in particular, is believed to have accounted for at least 30% to 50% of all central bank purchases over the past two years. The trend of diversifying away from the US dollar in more countries further enhances the attractiveness of this precious metal.

Moreover, weaker US economic data have raised hopes for interest rate cuts by the Federal Reserve, thereby boosting gold and silver prices. Additionally, despite the growth in stock markets, there is an underlying sense of doubt, which further supports gold and silver prices. From a technical standpoint, XAUUSD continues to exhibit a bullish trajectory.

Oil prices saw an uptick driven by optimistic data from China and the Eurozone, coupled with a decrease in US inventories reported in both the API and EIA weekly reports. Both WTI and Brent Oil concluded the week with gains ranging from 0.9% to nearly 1%.

The rollout of additional stimulus measures by China provided a significant boost to hopes for firmer demand in the energy market. Moreover, the simplification of home buying rules in China, alongside positive inflation data, further supported the upward momentum in oil prices. However, despite the support from US inflation data, this gain was somewhat tempered by a series of warnings from Fed officials cautioning that the central bank required more compelling data before considering rate adjustments.

Looking ahead to the coming week, we anticipate mostly positive data from the Eurozone and Asia, which is expected to sustain positive sentiment in the energy market. From a technical perspective, WTI retains its bullish stance, with 79.10 serving as its initial support level, while the key pivot point rests at 78.10

Cryptocurrency

Bitcoin’s price has surged above $65,000, propelled by factors such as slower US inflation and a weaker US dollar. This upward trend may persist, particularly as long as it remains above $62,000, with a weekly target of $71,000 for bullish momentum to continue.

Conversely, recent developments such as the Bitcoin halving and increased network complexities, coupled with regulatory uncertainties, have led to a decline in capital inflows into crypto investment products. In the upcoming week, with no significant events or market-moving data on the horizon, investors will need to closely monitor trends and news to navigate the market.

Share

Hot topics

Moving average Indicator (MA): Complete Guide for Traders

Introduction If you’ve ever looked at a price chart and wondered how quickly prices move, you’re not alone, especially if you’re still learning What Is Forex and How Does It...

Read more

Submit comment

Your email address will not be published. Required fields are marked *