Global Economic Outlook for 2025 | Regional and Global surveys

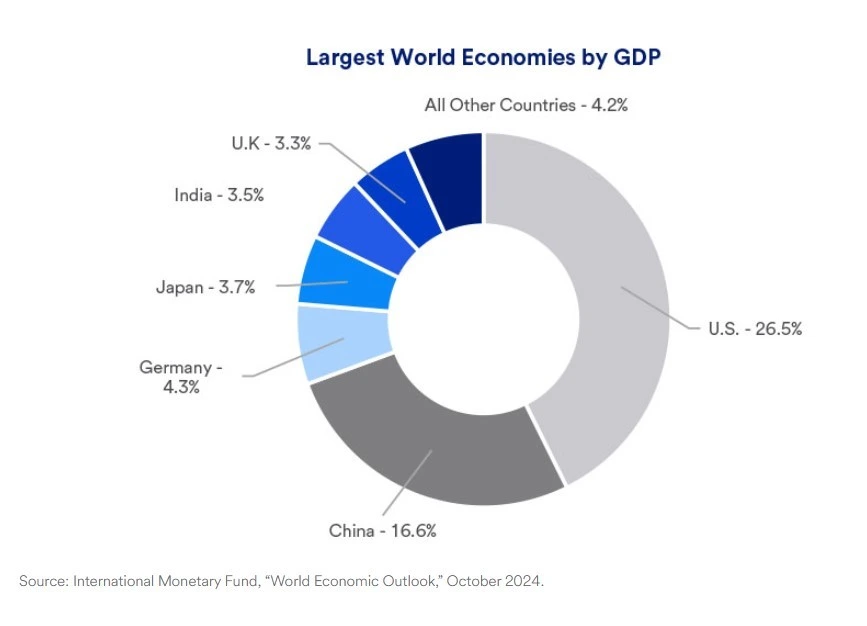

The global economic growth forecast remains stable, with projections of 3.1% for 2024 and 3.0% for 2025. The US economy is expected to grow by 2.8% in 2024 and 2.2% in 2025, supported by robust second-half growth in 2024. Japan’s growth outlook remains modest, with 0.1% in 2024 and a slight improvement to 1.0% in 2025. The Eurozone maintains forecasts of 0.8% for 2024 and 1.2% for 2025, while China is expected to grow by 4.9% in 2024 and 4.7% in 2025. India’s strong performance continues, with growth projections of 6.8% for 2024 and 6.3% for 2025. Brazil’s forecast is adjusted to 3.1% for 2024, holding steady at 2.1% for 2025, and Russia remains unchanged at 3.5% for 2024 and 1.7% for 2025.

Global forecasts from key institutions reveal diverse perspectives. Goldman Sachs predicts solid global growth in 2025, with US GDP increasing by 2.5% and the euro area expanding by 0.8%. Morgan Stanley projects global growth at 3% but anticipates a slowdown in the US due to tariffs and immigration policies. BNP Paribas highlights uncertainties from trade policies and geopolitical tensions.

Regionally, the Eurozone’s recovery is driven by rising household incomes and improved financing conditions, despite high energy costs and demographic challenges. The UK is forecast to grow by 1.5% in 2025, with inflation nearing 2%, while China faces deflationary pressures and risks from tariffs. Japan shows progress in overcoming its deflationary period, with inflation around 2%. Emerging economies have policy flexibility, though China’s performance affects overall growth. The global outlook reflects cautious optimism amid persistent challenges and opportunities across regions.

In the remainder of this article, we will delve into the economic outlook of key global regions, analyzing their specific growth trends, challenges, and opportunities. Additionally, we will explore the anticipated price behavior in the stock and currency markets within these regions, offering insights into potential market dynamics and investment implications.

The US Economy: Resilience Amid Uncertainty in 2024

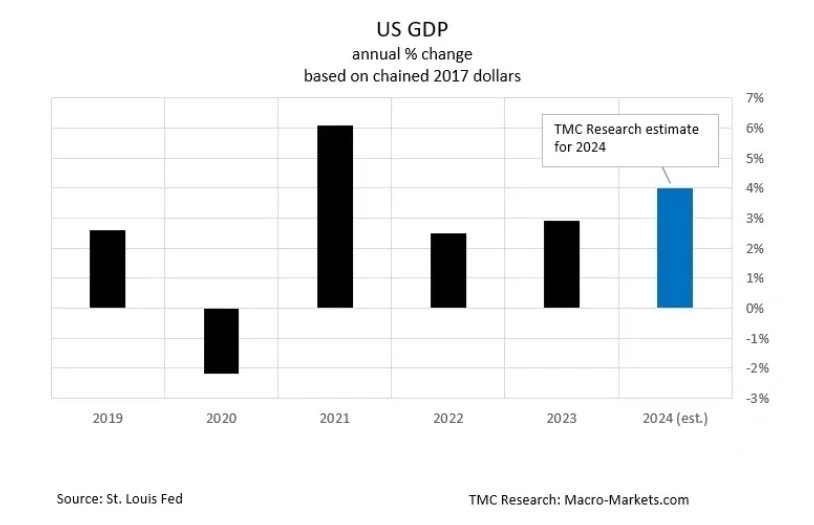

The US economy demonstrates remarkable resilience, driven by robust employment growth, strong consumer spending, and steady productivity gains. In 2024, employers added approximately 2 million jobs, and unemployment remained low, contributing to the country’s economic momentum. Real GDP growth is projected to reach 4.0% in 2024, marking the strongest expansion since 2021. However, challenges such as inflationary pressures and policy uncertainties linger, shaping the outlook for 2025.

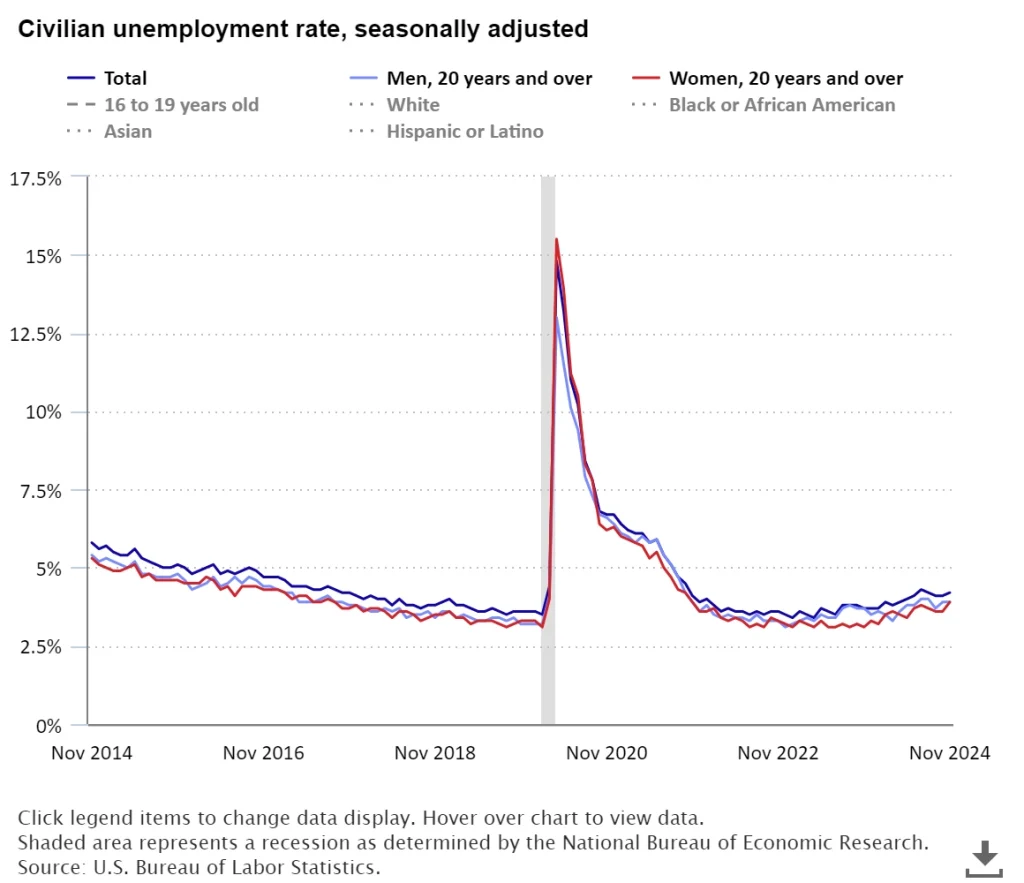

The labor market, while strong, is showing signs of cooling. November’s employment report highlighted a temporary rebound in payroll gains to 227,000 jobs following disruptions from strikes and natural disasters. However, the unemployment rate rose to 4.25%, reflecting softer labor conditions. Slowing labor supply, coupled with sticky wage growth of around 4%, indicates a more cautious hiring environment. Businesses are expected to curb wage increases, implement strategic layoffs, and focus on productivity improvements to manage costs.

The unemployment rate changed a little to 4.2 percent in November 2024. Among the major worker groups, the unemployment rate for Blacks (6.4 percent) edged up in November. The jobless rates for adult men (3.9 percent), adult women (3.9 percent), teenagers (13.2 percent), Whites (3.8 percent), Asians (3.8 percent), and Hispanics (5.3 percent) showed little or no change over the month.

The number of people employed part-time for economic reasons changed little to 4.5 million in November. This measure is up from 4.0 million a year earlier. These individuals would have preferred full-time employment but were working part-time because their hours had been reduced or they were unable to find full-time jobs.

The number of people in the labor force who currently want a job, at 5.5 million, changed little in November. These individuals were not counted as unemployed because they were not actively looking for work during the 4 weeks preceding the survey or were unavailable to take a job.

The US consumer engine, a key driver of economic growth, has shown signs of bifurcation. Real consumer spending grew by a modest 0.1% month-over-month in October, following stronger growth earlier in the year. Slowing labor market trends and elevated prices are expected to weigh on consumer spending, particularly for lower- to median-income households facing higher debt burdens and reduced savings.

Retail sales in the US increased 0.7% mom in November 2024, following an upwardly revised 0.5% rise in October and above forecasts of 0.5%. The data continued to point to robust consumer spending during the holiday shopping season. The biggest increases were recorded for sales of motor vehicles and pa… more.

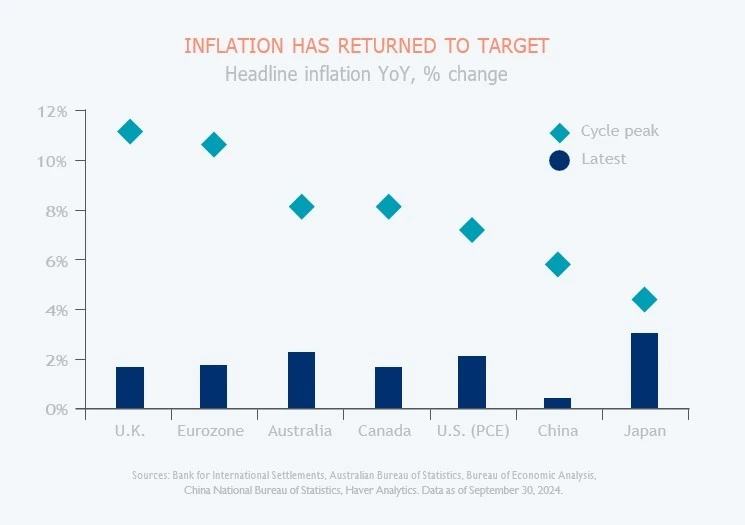

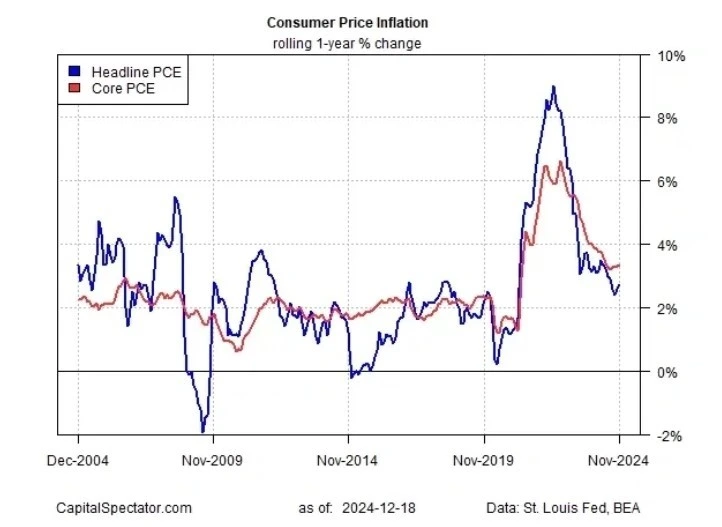

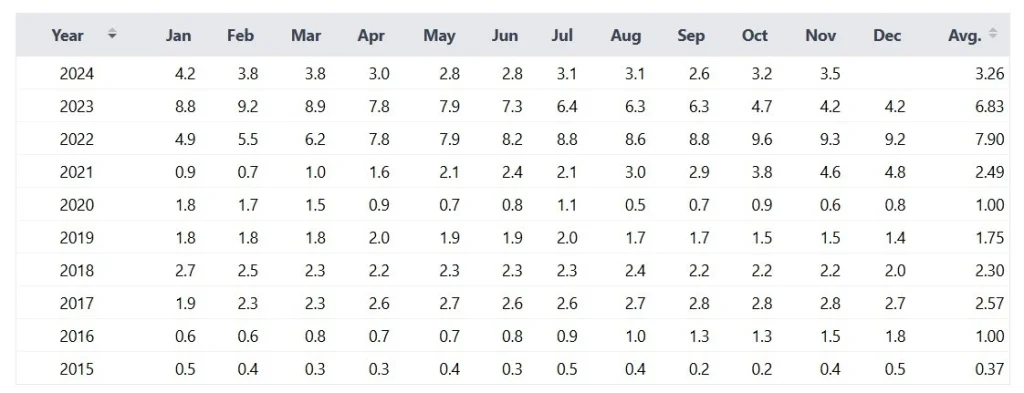

On the inflation level front, progress in taming price pressures has been uneven. Headline CPI inflation reached 2.7% year-over-year in Q4 2024 but is expected to ease to 2.2% by Q4 2025. Factors such as deregulation, potential immigration restrictions, and tariffs could introduce renewed inflationary risks in the medium term. These pressures, coupled with fragile supply conditions and geopolitical tensions, may define a “new normal” for inflation dynamics in the coming years.

US financial markets outperformed global counterparts in 2024, with stocks surging approximately 28%. This performance reflects robust economic growth and favorable market sentiment. The momentum is expected to carry into early 2025, though uncertainties surrounding trade policies, tariffs, and geopolitical tensions could introduce volatility.

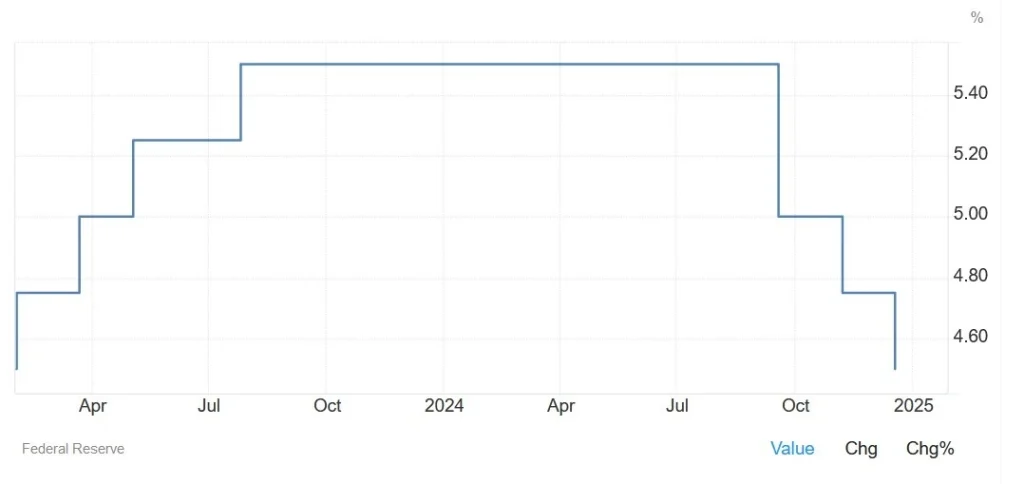

Federal Reserve Review: FOMC Policies and Decisions in 2024 and the 2025 Outlook

The Federal Reserve’s Federal Open Market Committee (FOMC) faced a complex economic environment in 2024, marked by persistent inflationary pressures, strong labor market dynamics, and robust economic growth. The central bank’s policy decisions reflected its dual mandate of achieving maximum employment and price stability as it navigated the challenges of moderating inflation without stifling economic momentum.

At the start of 2024, the Federal Reserve maintained a cautious stance, holding the federal funds rate steady after a series of rate hikes in 2022 and 2023 to combat inflation. By mid-year, as inflationary pressures began to show signs of easing, the FOMC hinted at a potential rate cut in May but refrained from acting. These signals were part of a gradual easing cycle designed to support the economy amid moderating inflation and cooling labor market conditions.

The FOMC initiated rate cuts on September 18 with a surprising 50 basis-point (bps) reduction. Two subsequent cuts, each by 25 bps in November and December, brought the total rate reduction to 100 bps for the year. The FOMC acknowledged that while progress had been made in taming inflation, the road to the 2% target would likely remain uneven, particularly given geopolitical risks and potential supply chain disruptions.

These decisions were influenced by:

- Persistent Inflationary Pressures: While headline inflation eased from its peak, core inflation remained elevated, requiring careful adjustments to avoid reigniting price pressures.

- Strong Economic Growth: Robust GDP growth, estimated at 4.0% for 2024, provided room for cautious rate adjustments without risking economic contraction.

- Labor Market Dynamics: The unemployment rate edged higher to 4.2% by year-end, signaling a cooling labor market without a sharp downturn.

Balance Sheet Policy

In addition to rate decisions, the Federal Reserve continued managing its balance sheet through a measured approach to quantitative tightening (QT). The FOMC allowed a limited amount of Treasury securities and mortgage-backed securities to mature without reinvestment, gradually reducing the balance sheet. This policy aims to normalize liquidity conditions in financial markets while avoiding undue pressure on economic growth.

The Federal Reserve’s policies in 2024 reflected a careful balancing act between managing inflation and supporting economic growth. The FOMC’s cautious easing cycle, combined with a measured approach to balance sheet normalization, demonstrated its adaptability in a challenging macroeconomic environment.

FED Outlook in 2025

Looking ahead to 2025, the FOMC’s forward guidance signals a cautious approach, with further rate cuts likely contingent on continued progress in reducing inflation and maintaining economic stability. Policymakers acknowledge the risks associated with geopolitical tensions, trade uncertainties, and structural changes in the labor market, underscoring the need for flexibility in monetary policy.

As Fed Chair Jerome Powell recently noted, a resilient US economy allows the Fed to adopt a measured approach to its rate-cutting cycle. Given cooling labor market conditions, strong productivity growth, and moderating inflation trends, a rate cut of at least 50 bps is anticipated during the 2025 meetings, down from the 100-bps reduction seen in 2024. Thereafter, the Fed is expected to slow the recalibration process in 2025 as policymakers aim for a neutral policy stance while navigating potential upside risks to inflation.

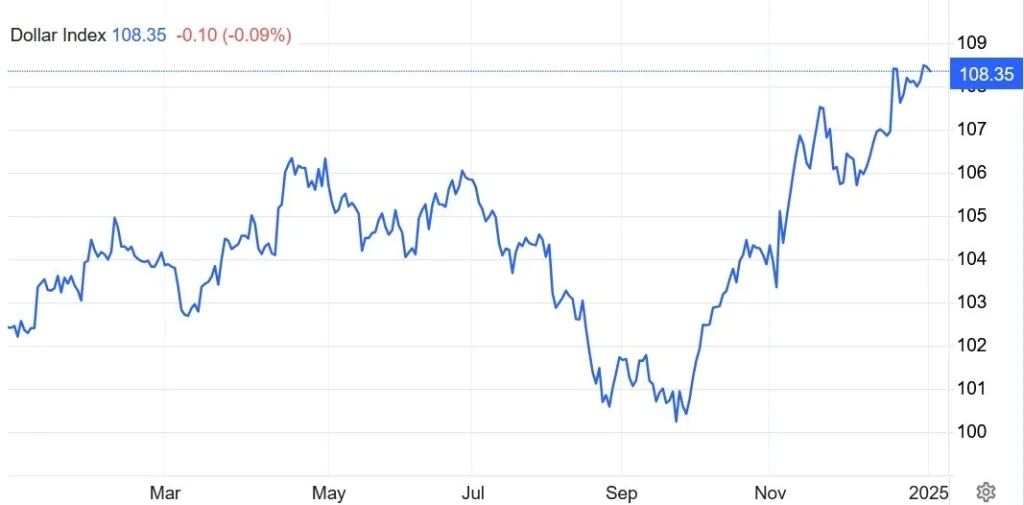

USD Review in 2024 and its Outlook for 2025!

The United States Dollar Index (DXY) measures the performance of the dollar against a basket of currencies, including the EUR, JPY, GBP, CAD, CHF, and SEK. The euro constitutes the largest component of the index, accounting for 57.6%, followed by the yen (13.6%), the pound (11.9%), the Canadian dollar (9.1%), the Swedish krona (4.2%), and the Swiss franc (3.6%).

The US dollar experienced a dynamic year in 2024, shaped by robust domestic economic performance, monetary policy adjustments, and evolving global market conditions. While the dollar demonstrated resilience and strength for much of the year, its trajectory was influenced by both external and internal economic factors. The dollar strengthened by approximately 7% against a basket of major currencies, buoyed by the Federal Reserve’s cautious approach to interest rate cuts amid persistent inflationary pressures. The dollar also benefited from former President Trump’s imminent return to the White House, as his proposed policies—such as deregulation, tax cuts, higher tariffs, and stricter immigration measures—were perceived as growth-oriented. Additionally, concerns about slower growth in other major economies and ongoing geopolitical risks contributed to safe-haven flows into the dollar.

The US economy expanded at an impressive 4.0% in 2024, its fastest pace since 2021. Robust consumer spending, strong business investments, and favorable labor market dynamics bolstered the dollar’s appeal. The United States’ economic outperformance relative to other major economies made the USD a preferred safe-haven currency, particularly during periods of global market uncertainty.

The Federal Reserve’s monetary policy decisions were pivotal in shaping the USD’s performance. The year began with the Fed holding interest rates steady. However, a surprising 50 basis-point rate cut in September, followed by two 25 basis-point cuts in November and December, marked the start of an easing cycle aimed at supporting the economy amid moderating inflation. While these rate cuts initially weighed on the dollar, strong economic fundamentals and sustained investor confidence helped mitigate its decline.

Geopolitical tensions and trade uncertainties also significantly influenced the dollar in 2024. As a safe-haven currency, the USD benefited from global events that heightened economic risks, such as conflicts and trade negotiations. Additionally, shifts in trade policies under the incoming Trump administration, including its stance on NATO and other international alliances, generated volatility but further reinforced the dollar’s status as a refuge asset.

The monetary policy divergence between the US and other economies further supported the USD. While the Federal Reserve adopted a cautious easing approach, several other central banks, including the European Central Bank and the Bank of Japan, maintained highly accommodative policies or introduced additional stimulus measures. This divergence widened interest rate differentials in favor of the US dollar, enhancing its attractiveness to international investors.

Performance Against Major Currencies

- Euro (EUR/USD): The dollar remained strong against the euro throughout 2024, supported by the US economy’s superior performance and ongoing challenges in the Eurozone, including slower growth and persistent inflationary pressures.

- Japanese Yen (USD/JPY): The dollar appreciated against the yen, as Japan maintained ultra-loose monetary policies, further widening yield differentials between the US and Japan.

- British Pound (GBP/USD): The dollar showed mixed performance against the pound. UK-specific risks, such as stagnant economic growth and political uncertainties, contributed to the pound’s weakness.

- Emerging Market Currencies: The USD generally appreciated against emerging market currencies, as heightened global uncertainty led to risk-off sentiment and capital flows into the relative safety of the US dollar.

Outlook for the US Dollar in 2025

As the Federal Reserve continues its cautious easing cycle in 2025, the dollar’s trajectory will likely depend on several key factors:

1. US Economic Momentum: Economic growth and progress in reducing inflation could support the dollar, even amid rate cuts.

2. Global Economic Developments: A potential slowdown in global growth or renewed geopolitical tensions could enhance the dollar’s safe-haven appeal. However, if President-elect Donald Trump successfully resolves tensions and ends the conflicts in Ukraine and the Middle East, this outlook may shift.

3. Policy Divergences: Continued divergence between US and global monetary policies may provide additional tailwinds for the USD. Eurozone economic growth still faces significant challenges, which could push the European Central Bank (ECB) to implement further rate cuts. This would widen the interest rate spread between central banks, boosting the USD against the euro and other currencies.

While the dollar faces challenges from potential tariff policies and geopolitical risks, its status as a global reserve currency and a safe-haven asset ensures it remains a key player in international financial markets.

Although much analysis emphasizes maintaining or strengthening the dollar, many overlook a critical aspect of Trump’s economic agenda: addressing the trade imbalance by reducing imports and increasing exports. Achieving this goal would likely require a weaker dollar, a priority for the new administration. Consequently, contrary to many forecasts, the dollar may not perform as strongly in 2025 as it did in 2024.

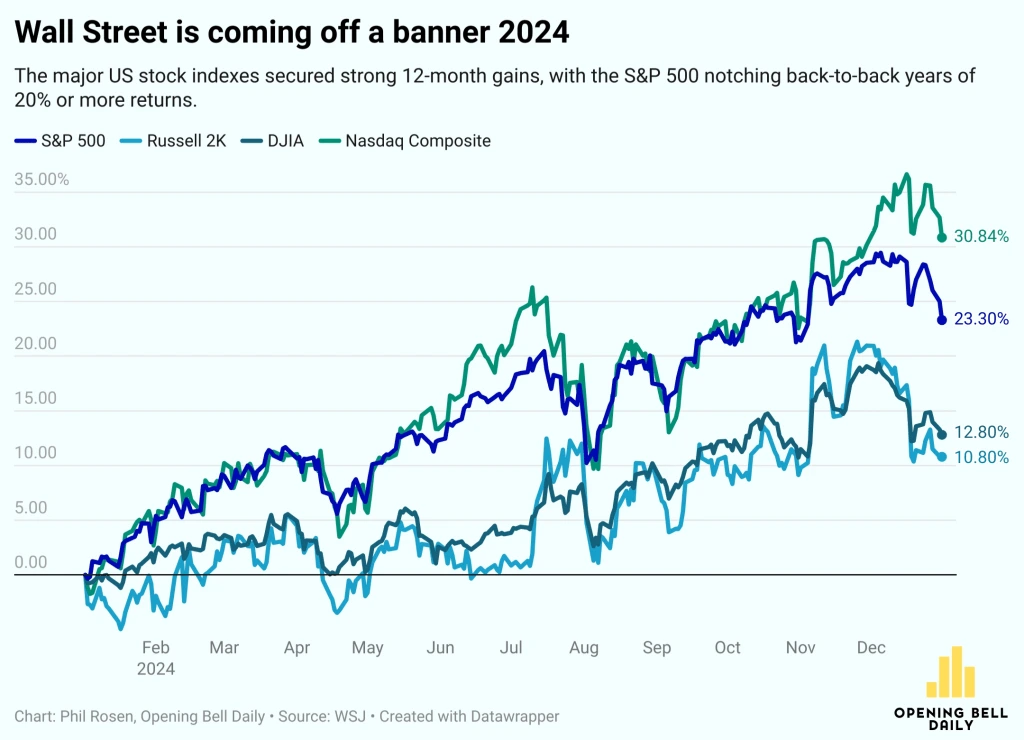

Wall Street: 2024 Review and Future Expectations

Wall Street demonstrated remarkable strength in 2024, defying expectations and navigating a complex global and domestic landscape. Major indices posted impressive gains, driven by robust economic growth, technological innovation, and key monetary policy decisions. The S&P 500 rose by 23.3%, achieving its best two-year performance since 1997-1998. The Nasdaq Composite surged 28.6%, fueled by technology and consumer discretionary stocks, while the Dow Jones Industrial Average advanced 12.9%, contributing to overall market optimism.

A significant driver of Wall Street’s success was the explosion of artificial intelligence, with innovations in AI and cloud computing propelling technology stocks to new heights. Communication services and consumer discretionary sectors also experienced substantial growth, with gains ranging from 29.1% to 38.9%. The U.S. economy expanded at an impressive 4.0%, supported by strong consumer spending, increased business investment, and a resilient labor market. These factors bolstered corporate earnings, particularly in the technology, healthcare, and consumer sectors, fostering investor confidence and driving equity prices higher.

The Federal Reserve’s monetary policy played a crucial role in shaping market dynamics. Rate cuts implemented in the latter half of the year reassured investors that inflation was being managed without jeopardizing economic growth. Despite initial concerns, the Fed’s cautious approach provided stability for the markets. The political landscape also influenced Wall Street’s trajectory. Donald Trump’s re-election in November fueled market enthusiasm, with expectations of pro-growth policies such as deregulation and tax reforms driving investor optimism. The year also saw cryptocurrencies gain prominence, with Bitcoin surging 122% amid heightened interest in alternative investments.

Although Wall Street’s performance was robust, it was not without challenges. Geopolitical tensions, including ongoing conflicts in Ukraine and the Middle East, created periods of uncertainty, occasionally weighing on investor sentiment. Speculation about the Federal Reserve’s future policy path introduced elements of caution, while a year-end decline of 1.6% in the S&P 500 marked the worst year-end performance since 1952.

The IPO market experienced a resurgence in 2024, particularly in the technology and green energy sectors, reflecting strong investor appetite for growth-oriented companies. However, market breadth showed mixed results, with advancing stocks outnumbering decliners on the NYSE, while Nasdaq saw more declining issues.

In summary, Wall Street’s remarkable performance in 2024 highlighted its resilience amidst a backdrop of economic growth, innovation, and global challenges. As the stage is set for 2025, investors remain optimistic but cautious, mindful of evolving geopolitical risks, potential shifts in monetary policy, and global economic uncertainties.

Outlook for Wall Street in 2025:

Wall Street enters 2025 with cautious optimism. Potential catalysts include continued innovation in technology, progress in resolving geopolitical conflicts, and the potential for further fiscal and monetary policy adjustments. However, challenges like a potentially weaker dollar, evolving trade policies, and slower global growth may create headwinds for the market.

Wall Street’s predictions for 2025 are heavily influenced by the return of Donald Trump to the White House, with many financial institutions optimistic about his pro-business policies. This optimism is especially focused on U.S. assets and Corporate America, as Trump’s policies are expected to drive growth. However, his tough stance on global trade and unpredictability are causing some concerns.

The U.S. economy is expected to continue thriving, benefiting from Trump’s policies and the relative lack of appeal of other major markets, which could be impacted by his trade barriers. Inflation is seen as contained but unlikely to meet target levels due to Trump’s trade and immigration policies. Many analysts anticipate that interest rates will be cut more slowly than expected.

While there are some financial institutions caution against expecting another year of 20% equity returns, they remain optimistic about the ongoing artificial intelligence boom. Technology gains are expected to broaden as AI adoption continues to grow. Bond yields are solid but not expected to be a major investment focus, given concerns about government borrowing. Diversification into alternative assets like private markets and hedge funds is encouraged to navigate the uncertain landscape.

Overall, Wall Street remains focused on Trump’s influence, U.S. economic strength, and the evolving tech landscape, with a sense of cautious optimism tempered by global uncertainties and market volatility.

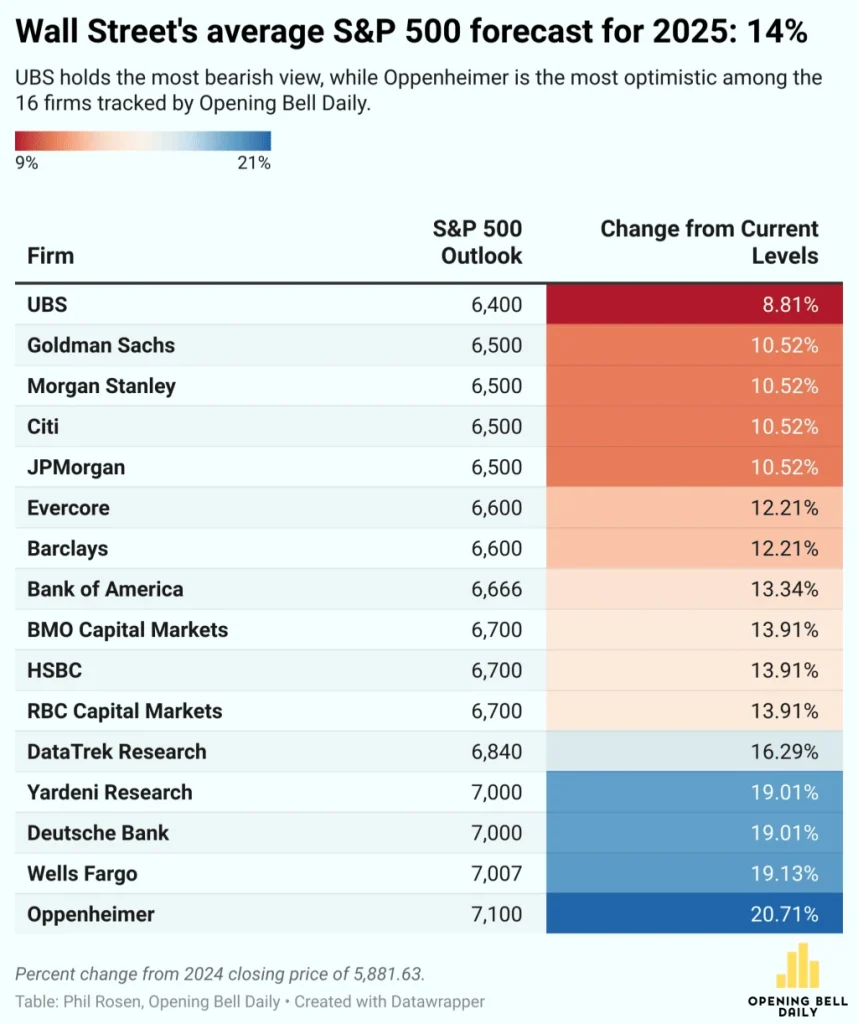

The stock market in 2025 is expected to be driven by corporate earnings, with Wall Street optimistic about growth despite a mixed economic outlook. The S&P 500 ended 2024 with a 23.3% return, and analysts are forecasting a 14.8% year-over-year earnings growth rate for 2025, well above the 10-year average of 8%. While major tech companies (the “Magnificent 7”) are expected to see a 21% earnings growth, analysts anticipate a narrowing of the gap with the rest of the companies at the S&P 500, which are expected to grow earnings by 13%.

Goldman Sachs forecasts a 10% rise in the S&P 500, noting that as earnings growth broadens, big tech’s dominance may diminish. Both revenue growth and profit margins are expected to surpass their 10-year averages. Overall, the outlook for Wall Street is positive, with an average forecast of a 14.03% increase in S&P 500 over the next year.

However, we should not forget about challenges that may Face by Wall Street, such as:

Inflation and Fed Policy: While inflation cooled, concerns over its persistence led to cautious optimism. The Federal Reserve’s rate cuts provided relief but also raised questions about the economy’s underlying strength.

Debt Markets: Rising government debt levels and potential fiscal constraints created uncertainties in fixed-income markets, impacting equity performance indirectly.

Eurozone, Overall Condition, and 2025 Outlook!

In 2024, the Eurozone’s economic performance faced a mixture of challenges and modest recovery, influenced by both global and regional factors. Growth was generally subdued, with a notable decline in momentum compared to previous years. The Eurozone’s economy struggled to achieve robust growth in 2024, with an overall growth rate projected to be below 1%. The region continued to grapple with a slow recovery from the disruptions caused by the pandemic and geopolitical tensions. A combination of factors, including rising inflationary pressures and global supply chain disruptions, weighed on consumer spending and business investment.

Inflation remained a key concern for the Eurozone economy throughout 2024, though it showed signs of moderation compared to previous years. The European Central Bank (ECB) faced a delicate balancing act, attempting to control inflation without stifling growth. Interest rate hikes continued as part of the ECB’s efforts to curb rising prices before they started cutting the rates in the last quarter.

The Eurozone was impacted by global trade conditions, particularly the fallout from great economic growth in the United States and ongoing economic and financial challenges in China.

The Eurozone’s trade balance was further strained by volatility in commodity markets, particularly energy prices, which fluctuated due to geopolitical uncertainties and supply issues. Despite this, the region’s export-driven industries, particularly in Germany, saw some relief from strong demand in emerging markets. The German economy experienced one of the worst economies among developed economies in 2024.

On the political front, concerns continue. The political landscape in the Eurozone remained unstable in 2024. The fragmentation of political systems in major economies like Germany and France exacerbated the economic challenges, leading to delays in necessary reforms and investments. For example, Germany faced continued political uncertainty as coalition talks dragged on, dampening investor confidence. With the upcoming election in Germany, this condition can continue further, while France also does not have any better conditions. Germany likely experience instability until post-election in February 2025 and France will face political deadlock until 2027. European stock markets have underperformed compared to the US, and while some see potential for recovery after the German elections, caution remains.

Despite the economic headwinds, the Eurozone labor market was resilient in 2024. Unemployment rates continued to fall, but the quality of jobs remained a concern, with many countries facing a rise in part-time and low-wage employment. However, certain sectors, such as technology and green energy, benefited from government policies to foster job creation in emerging industries.

The Eurozone’s banking sector remained cautious in 2024, with banks maintaining tight lending standards amidst uncertainty. However, the financial services sector, particularly fintech, showed resilience, benefiting from the European Union’s supportive regulatory framework. Investment in innovation and digital transformation, especially in fintech, AI, and green technologies, offered hope for future growth.

Eurozone 2025 Economic Outlook

Overall, the Eurozone’s economy in 2024 was marked by slow growth and ongoing vulnerability to external and internal challenges. While the region’s economic performance showed signs of stability, the outlook for 2025 remains uncertain, with political fragmentation, trade tensions, and inflationary pressures continuing to pose risks to the region’s economic recovery. While the Eurozone avoided a sharp recession, its economic growth in 2024 was tepid at best. The focus for policymakers in 2025 will need to be on stabilizing growth, navigating trade tensions, and addressing political fragmentation to secure a more robust recovery.

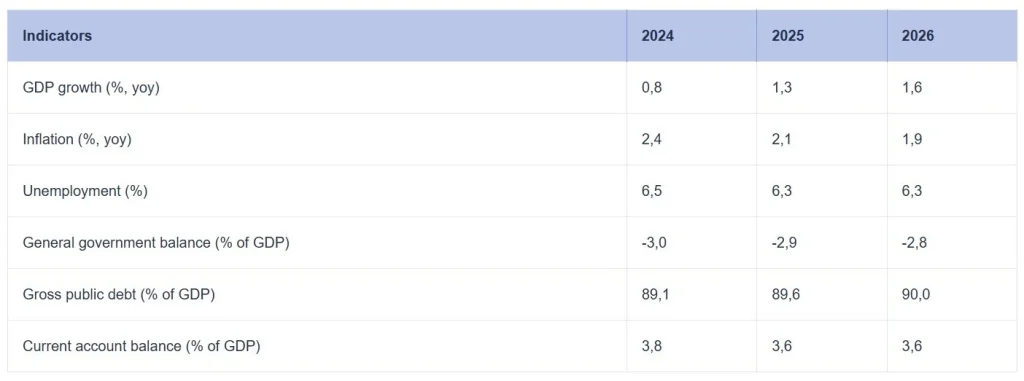

The Eurozone faces significant challenges in 2025, including trade wars and political instability. US protectionist policies, particularly potential tariffs of up to 20% on imports, threaten the Eurozone’s trade surplus, potentially triggering retaliatory actions. Economic growth is projected to be weak, with a growth forecast of just 1.1%, and the Eurozone’s economy could even contract by 1% if tariffs are implemented.

The Eurozone’s GDP growth is projected to be 0.8% in 2024 and 1.2% in 2025, with Germany underperforming compared to other Eurozone countries, while Spain continues to perform well. The slight revision to growth forecasts is mainly due to past data updates. Inflation in 2024 is expected to be marginally lower than anticipated (2.4% vs. 2.5%) due to a more significant drop in energy prices.

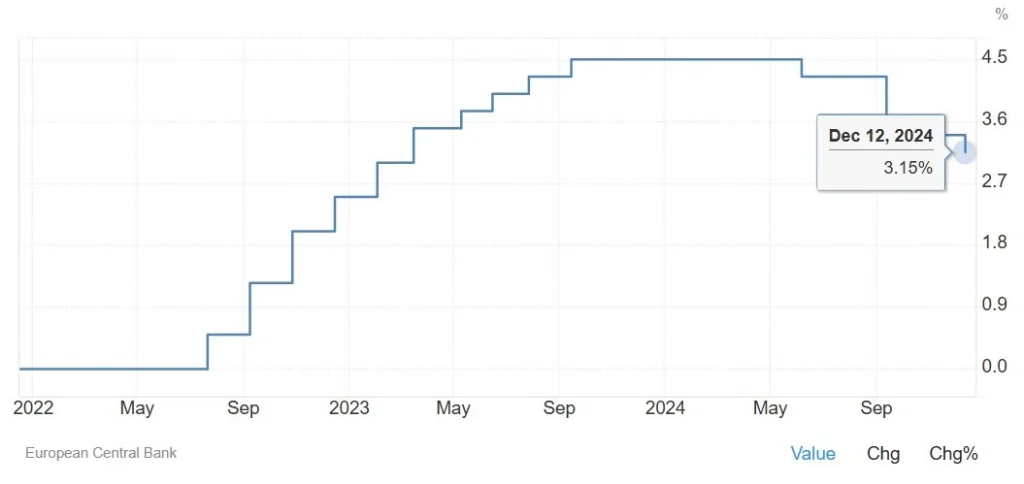

A shift in macroeconomic stability is expected, as new leadership in the U.S., EU, and Germany could lead to decisions on tariffs, defense, and spending that reshape the economic outlook. The European Central Bank (ECB) is anticipated to cut rates more quickly than originally forecasted, with the main policy rate expected to reach 2.5% by summer 2025, ahead of the previous estimate of September 2025. Overall, the Eurozone’s economic outlook remains relatively stable, with modest growth and inflation expectations. Germany’s growth is expected to lag, while Spain will continue to outperform.

Headline inflation in the Eurozone is projected to increase slightly in the last quarter of 2024 but is expected to decline and stabilize around the European Central Bank’s (ECB) 2% target by the second quarter of 2025. The rise in inflation towards the end of 2024 is mainly due to base effects from energy prices, followed by a downward trend. HICPX inflation (excluding energy and food) is expected to decline from 2.9% in 2024 to 1.9% by 2027, largely driven by moderation in services inflation.

While services inflation has remained persistent around 4% since November 2023, a decline in services inflation and easing labor cost pressures are expected to contribute to the decrease in HICPX inflation from early 2025. The disinflation process will also reflect the continued effects of past energy price shocks and the ECB’s monetary policy measures between December 2021 and September 2023. A small temporary rise in inflation is anticipated in 2027 due to fiscal measures related to the green transition, but overall, inflation is expected to gradually decline over the projection period.

Net trade is expected to have a neutral impact on GDP growth, despite ongoing competitiveness challenges. The unemployment rate is anticipated to decline further to historically low levels. As cyclical factors that have recently reduced productivity unwind, productivity is expected to improve, though structural challenges persist. Real GDP growth is projected to be 0.7% in 2024, 1.1% in 2025, 1.4% in 2026, and 1.3% in 2027. This forecast is lower than the previous September 2024 ECB projections, primarily due to revised investment data for the first half of 2024, weaker export growth expectations for 2025, and a slight downward revision of domestic demand growth for 2026.

S&P Global Ratings expects the European Central Bank (ECB) to now slash interest rates quicker than anticipated, mainly because of ongoing dampened confidence, as well as more data supporting disinflation progress. The main policy rate is expected to now touch 2.5% before next summer, significantly ahead of S&P’s previous forecast for September 2025. Coming to how quicker rate cuts by the ECB might impact this outlook, Broyer said: “Faster rate cuts could help boost confidence, which remains surprisingly depressed despite the return of growth, disinflation, and full employment. As a result, faster rate cuts would support the recovery in consumer spending and investment, which remain the mainstays of the European recovery.”

Euro Outlook for 2025

The outlook for the EUR/USD currency pair in 2025 is influenced by several key factors, including economic performance, monetary policy decisions, and geopolitical developments in both the Eurozone and the U.S. Here’s an overview of the expected trends for EUR/USD in 2025.

The Eurozone is expected to experience modest GDP growth, while the U.S. economy may continue to show relatively stable growth. The divergence in growth rates between the Eurozone and the U.S. could lead to fluctuations in central bank’s policies and therefore their interest rates as well. A bigger spread between the ECB and Fed, can increase the carry trade and affect the EUR/USD pair, in favor of the USD.

As mentioned earlier, the ECB is expected to begin cutting interest rates more quickly than previously anticipated, with the main policy rate likely to reach 2.5% by mid-2025. A more dovish ECB stance in response to economic challenges and inflation moderation could weigh on the Euro, making it less attractive relative to the U.S. Dollar. The Federal Reserve is likely to maintain a cautious approach to interest rate cuts, as inflationary pressures may persist. If the Fed takes a more hawkish stance compared to the ECB, the U.S. Dollar could continue to benefit, potentially strengthening the USD relative to the Euro.

Additionally, geopolitical factors, including ongoing trade relations between the U.S. and the Eurozone, global tensions, and domestic political developments in both regions, could significantly impact the EUR/USD exchange rate. A resolution to trade disputes or any fiscal stimulus measures could influence market sentiment and the direction of the Euro.

In 2025, EUR/USD is likely to remain volatile, influenced by economic growth disparities, inflation dynamics, and differing monetary policies between the ECB and the Federal Reserve. While the U.S. Dollar may hold an advantage due to potentially stronger economic performance and a more hawkish Fed stance, any positive developments in the Eurozone, including recovery in key economies like Germany and Spain, or shifts in ECB policy, could provide support for the Euro, leading to a more balanced outlook for the currency pair under 1.10 USD for each Euro.

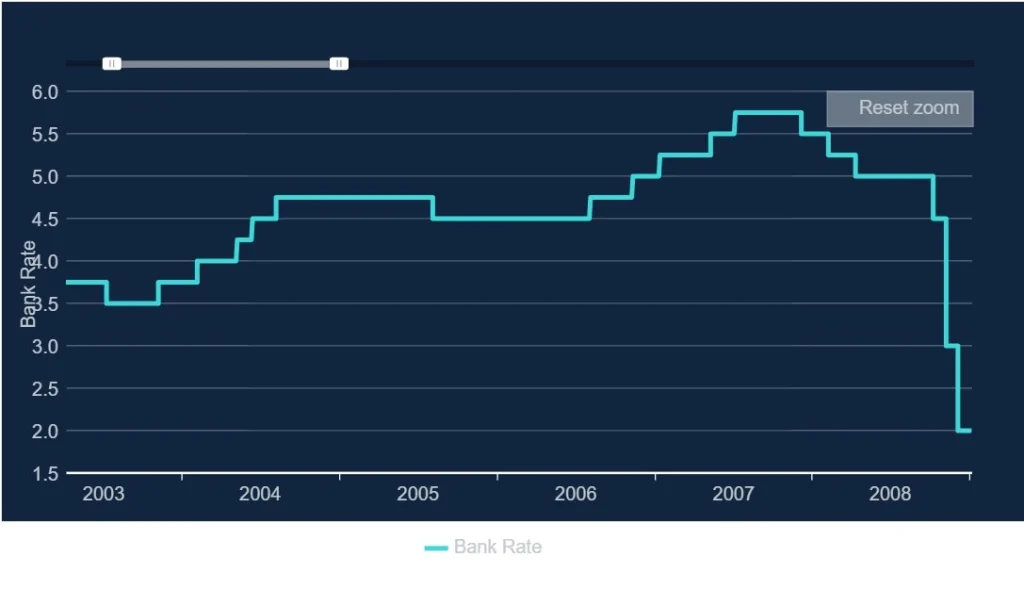

UK Economy During 2024 and 2025 Outlook

The UK economy in 2024 faced a mixture of challenges and gradual recovery. Growth remained modest, though the outlook was revised downward from earlier forecasts. GDP growth is estimated to be between 0.9% and 1.1% in 2024, reflecting weak domestic demand and global uncertainties. Key factors influencing this performance include ongoing inflationary pressures, geopolitical risks, and potential impacts from domestic political decisions, particularly those related to post-Brexit trade arrangements. Additionally, the Labor Party’s return to power after 14 years marked a significant political shift, with potential long-term economic implications.

Inflation eased sharply in 2024, declining from the high levels seen in 2023. However, despite this moderation, inflation remained above the Bank of England’s target of 2%, hovering closer to 3%. Persistent factors such as high energy costs, elevated food prices, and supply chain disruptions kept inflation elevated. Some further moderation is anticipated as energy prices stabilize and inflationary pressures continue to ease.

On the monetary policy and interest rate front, the Bank of England (BoE) adopted a cautious stance in 2024. While interest rates increased slightly early in the year, the pace of tightening slowed compared to previous years. As inflation showed signs of easing and economic growth remained sluggish, the BoE began considering rate cuts in the final quarter of 2024. These rate cuts could extend into early 2025, provided inflationary pressures subside sufficiently.

The UK labor market demonstrated resilience in 2024, with unemployment rates declining to 4.3%. However, wage growth lagged behind inflation, resulting in reduced real incomes for many workers.

Among developed economies, the UK recorded the weakest economic growth in 2024. This underperformance stemmed from a combination of inflationary pressures, subdued consumer spending, and modest business investment.

2025 Outlook for the UK Economy

Looking ahead to 2025, the economic outlook is slightly more optimistic, with growth expectations set at 1.5%. This improvement is partially attributed to fiscal easing measures introduced in the October 2024 budget. However, inflation remains a critical concern, projected to stay above the Bank of England’s target until mid-2026. The BoE’s cautious approach to rate cuts suggests a terminal interest rate of 3.5% by early 2026. While the economy may show signs of recovery, challenges persist, particularly with the new government’s budget plans.

External risks, such as potential tariffs imposed by the U.S. and ongoing global trade uncertainties, could complicate the UK’s economic trajectory. These factors may also contribute to increased volatility in currency and bond markets.

Sterling in 2025

UK interest rates are expected to decline gradually, bringing relief to mortgage rates. The Monetary Policy Committee is likely to reduce interest rates by at least 100 basis points over 2025, with the BoE Bank Rate projected to settle at 3.5%-3.75% by year-end. This lower interest rate profile, compared to market expectations, should help bring down mortgage costs.

However, this rate trajectory may exert downward pressure on the pound sterling, though its impact on the euro is expected to be less pronounced.

Japan: How Did the Economy Perform in 2024 and What Is the 2025 Outlook?

Japan’s Economic Performance in 2024

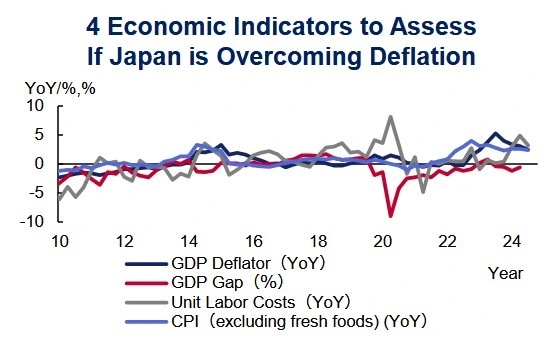

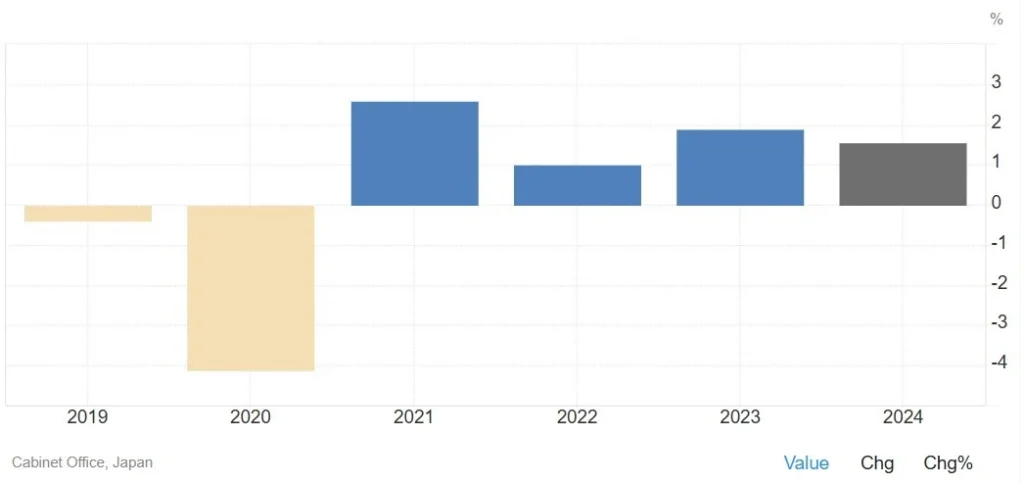

Japan’s economy in 2024 demonstrated a modest recovery, marking a transition from decades of deflation to steady growth. The real GDP growth rate for the year was supported by domestic demand, labor-saving investments, and a recovery in the tourism sector. Japan’s GDP growth is forecasted to be 1.55% in FY2024.

Consumer spending, or household consumption, played a critical role, driven by moderate wage growth and supportive fiscal policies. However, inflationary pressures posed challenges to purchasing power. To overcome supply shortages and balance the market, businesses increased capital investments in automation and digital transformation to address labor shortages and enhance productivity.

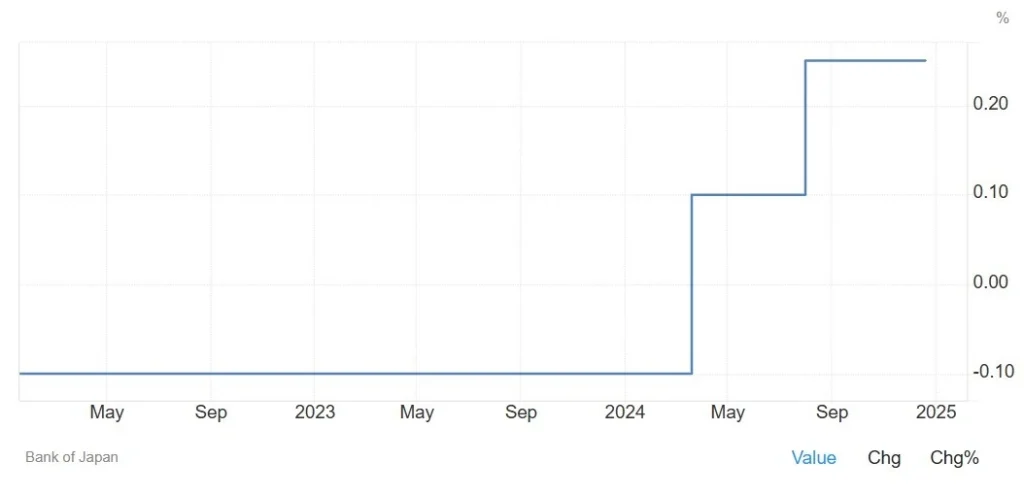

In the service sector, particularly in tourism, Japan experienced a surge in inbound foreign tourists, contributing to growth in the service industry and related sectors. The Bank of Japan (BoJ) played a very important role in supporting economic growth. It maintained an accommodative stance for most of 2024 but began signaling a gradual shift toward policy normalization later in the year. The Bank of Japan’s October 2024 Outlook Report anticipated that the economy would maintain growth above its potential rate, driven by moderate expansion in overseas economies and accommodative financial conditions.

Despite these positive trends and economic growth, especially stock market gains, challenges persisted. Inflation remained above the BoJ’s target for much of the year, and global economic uncertainties, including trade conflicts and slower growth in major economies like the U.S. and China, weighed on the export sector. Japan’s dependence on energy imports also exposed the economy to fluctuations in global energy prices.

Overall, Japan’s economic performance in 2024 was a balancing act between leveraging domestic strengths and navigating external challenges. Despite these hurdles, the Japanese economy demonstrated resilience, transitioning from deflation to a phase of steady growth and renewed corporate dynamism. The groundwork laid in 2024, particularly through structural reforms and monetary adjustments, has set the stage for continued recovery in 2025.

Japan 2025 Economic Outlook: Growth Amid Challenges

Japan’s economy is poised to continue its recovery in 2025, building on the positive momentum established in 2024. Growth is expected to be driven by strong domestic demand, increased labor-saving investments, and a resurgence in tourism. However, challenges such as persistent inflation, global trade uncertainties, and geopolitical risks loom large.

Japan’s real GDP growth is forecasted at 1.1% for 2025, a rate above its potential. Consumer spending, supported by wage increases and government measures, remains a central pillar of growth. The government has introduced fiscal policies, including tax reforms and subsidies, to stimulate consumption and ease household financial burdens, particularly on energy costs.

Corporate investments in automation, digital transformation, and decarbonization will address labor shortages and enhance productivity. Additionally, the tourism sector continues to recover, with inbound foreign visitors contributing significantly to service sector growth.

The Consumer Price Index (CPI), excluding fresh food, is projected to grow at 1.9% in fiscal 2025, slightly below the previous year’s 2.5%. Inflationary pressures are driven by improving wage growth and diminishing effects of past import price surges.

Labor market challenges remain a critical focus for 2025. Wage growth, which rose by 5.1% in 2024, —the highest in over three decades—will continue to drive household spending. However, structural labor shortages necessitate further investments in automation and reskilling programs to sustain economic momentum.

Japan’s financial markets are projected to perform strongly in 2025. The TOPIX index is expected to reach 3,000 points, buoyed by corporate governance reforms and increased share buybacks. The USD/JPY exchange rate is forecasted to stabilize at approximately 140 yen per dollar, reflecting steady monetary adjustments.

While interest rate hikes could challenge real estate financing, strong domestic demand and urban redevelopment projects are expected to offset these pressures.

Global trade uncertainties, particularly heightened tariffs from the US protectionist policies, pose risks to Japan’s export sector. Geopolitical tensions in East Asia and slower growth in major trading partners like the US and China add further complexity. Domestically, the fragmented political landscape may delay critical reforms, although balanced fiscal policies could emerge as a result. Japan’s dependence on energy imports also exposes it to fluctuations in global commodity prices, potentially straining corporate profits and household incomes.

On the policy front, the Bank of Japan (BoJ) began normalizing monetary policy in 2024, marking a historic shift after years of ultra-loose monetary measures. In 2025, the BoJ is expected to continue this trend, gradually increasing interest rates to 1% while adjusting its yield curve control measures. These steps aim to strike a balance between controlling inflation and supporting economic growth. The government is also implementing fiscal measures, including tax reforms and subsidies, to stimulate consumer spending and investment.

Japan’s outlook for 2025 reflects cautious optimism. The combination of supportive fiscal and monetary policies, rising wages, and structural reforms offers a solid foundation for growth. However, navigating global economic uncertainties and addressing domestic challenges will require adaptability and resilience.

By leveraging innovation, promoting green and digital transformation, and enhancing labor productivity, Japan aims to build a sustainable economic framework. These efforts position the country to capitalize on opportunities while mitigating risks in an increasingly complex global landscape.

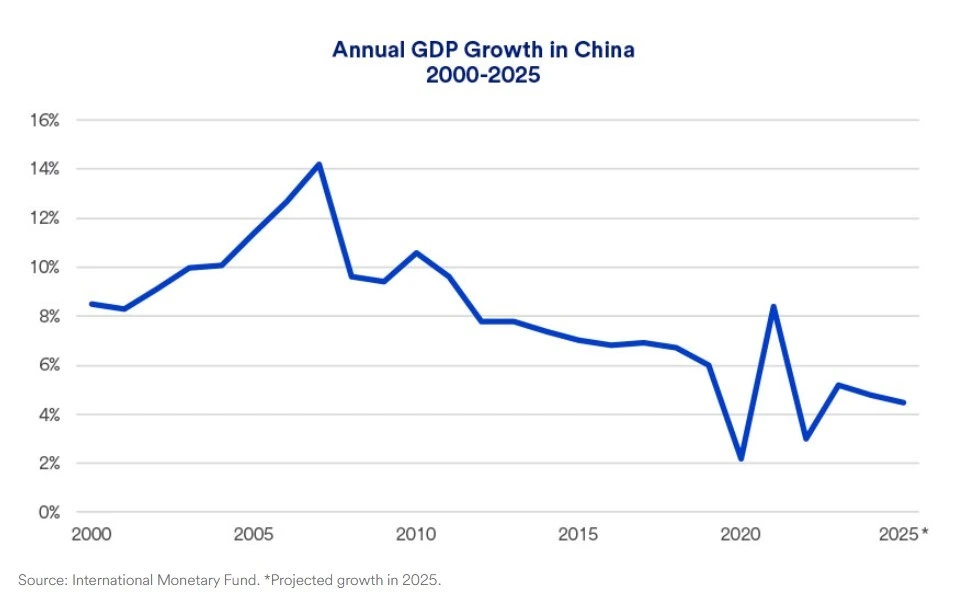

China’s Economy: 2024 Review and Outlook for 2025

China’s once high-flying economy continued to face significant headwinds in 2024, stemming from an overbuilt property sector, cautious consumer spending and heightened global trade tensions. While China averaged over 9% annual GDP growth between 2000 and 2019, its economic trajectory has slowed considerably in recent years. Since 2020, annual growth has averaged 4.7%, which is also the rate forecasted for 2024 by the International Monetary Fund (IMF).

China 2024 Economic Performance

The year 2024 marked another challenging period for China’s economy, as it struggled to recover from systemic issues in key sectors:

- The property sector’s collapse remains a major drag on growth. Millions of unfinished housing units and significant levels of debt have strained local governments and financial institutions. Despite the government’s stabilization measures, recovery has been slow.

- Structural barriers and persistent caution among consumers have hindered the shift to a consumption-driven growth model. While the government and central bank introduced stimulus measures earlier in the year, including support for household spending and debt restructuring, the lack of specific and actionable policies has tempered market optimism.

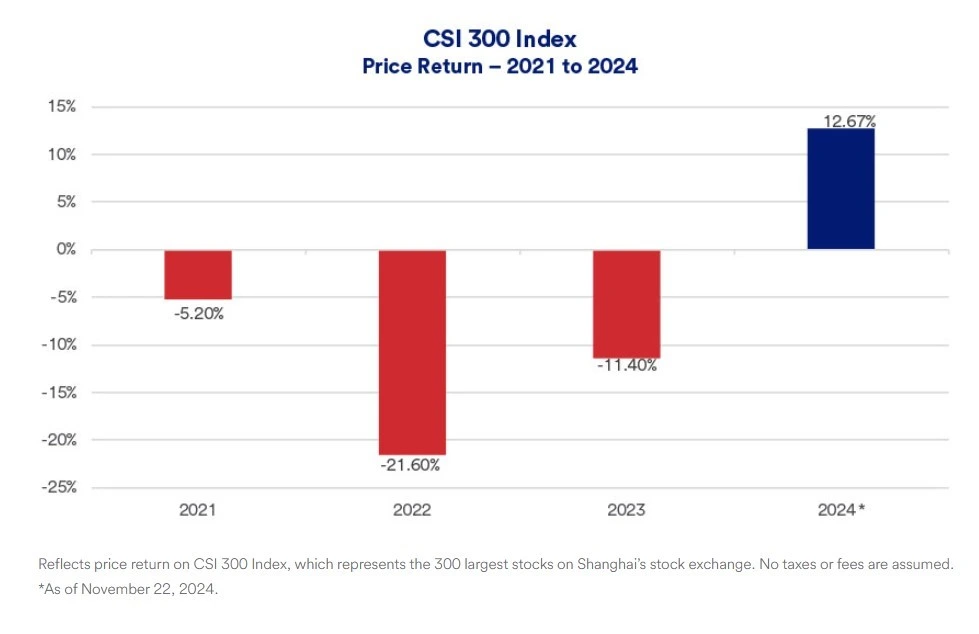

On the Stock Markets front, the CSI 300 Index, which tracks the largest 300 stocks on the Shanghai Stock Exchange, initially reacted positively to government stimulus, reaching a 24% year-to-date gain in early October 2024. However, disappointment in the measures’ lack of detail caused a retreat, and the index ended November with a 12.7% year-to-date gain. Despite this modest recovery, the CSI 300 remains 35% below its February 2021 peak.

While we have reviewed the relatively positive conditions, we should not ignore the structural and Global Challenges. China continues to rely heavily on exports to sustain its growth. However, rising trade tensions, particularly with the US and EU, have led to tariffs and restrictions on high-tech goods. These measures, coupled with geopolitical risks, pose significant challenges to China’s export-driven economy.

According to the domestic challenges, the Labor Market and Youth Unemployment are the key factors to watch. Structural mismatches in the labor market have resulted in rising youth unemployment, highlighting broader challenges in adapting to a modernizing economy. While banks remain heavily exposed to the property sector, limiting credit availability for productive investments. State-directed interventions aim to maintain financial stability but reveal underlying systemic risks.

China’s Economy in 2025

As we move into 2025, the door appears open to escalating trade tensions. President Trump heavily campaigned on imposing new tariffs on goods imported into the U.S., with a primary focus on China. The economic outlook for China in 2025 remains uncertain, though the groundwork laid in 2024 provides opportunities for stabilization. Key areas to watch include:

First, the government must prioritize stimulating domestic demand and consumption. Measures to boost household spending and confidence are expected to intensify in 2025. However, the effectiveness of these policies will depend on their specificity and implementation. Stronger policies are anticipated to increase household income and strengthen consumption capacity, aiming to bolster spending and expand effective domestic demand.

Property market stabilization could be a pivotal factor for China’s GDP and overall economic growth. Efforts to address the housing price overhang and excessive market debt are critical. While initial measures have shown limited success, further targeted interventions could help restore balance to this crucial sector.

With trade tensions likely to increase, China will also need a new export and trade strategy. Navigating global trade challenges and diversifying export markets will be essential. Investments in high-tech manufacturing, such as electric vehicles and solar panels, remain a bright spot, though they face growing competition and geopolitical resistance.

Another area requiring significant attention is China’s financial sector, government debt, and investment trends. Financial reforms will be critical to managing systemic risks, particularly overexpose to property-related debt, ensuring long-term stability. In 2025, China is expected to adopt a more proactive fiscal policy and shift to a moderately loose monetary stance after 14 consecutive years of maintaining a prudent monetary policy.

While the challenges ahead are substantial, there are opportunities for recovery if China can effectively balance domestic reforms with external trade strategies. As investors closely monitor government actions, the trajectory of China’s economy in 2025 will play a pivotal role in regional and global markets.

The annual Central Economic Work Conference, held in early December in Beijing, outlined priorities for China’s economic agenda in 2025. The meeting emphasized the importance of maintaining steady economic growth, ensuring stable employment and prices, achieving a basic equilibrium in the balance of payments, and increasing residents’ incomes in line with economic growth.

Share

Hot topics

Gold symbol in forex

Introduction If you have ever opened a trading platform and searched for gold, you probably noticed a specific code instead of the word “gold.” In the forex world, assets are...

Read more

Submit comment

Your email address will not be published. Required fields are marked *